Recommended Weekend Reads

The War on Ukraine, Broader Implications of the Peace Talks, Argentina’s Big Challenge, and the Future of Europe’s Security

March 14 - 16, 2025

Russia’s War on Ukraine and The Implications of a Possible Cease Fire

The Kremlin's Balancing Act Foreign Policy Research Institute

Following Russia’s invasion of Ukraine, the Russian government accelerated the preexisting trend of centralizing control over regional power and economic assets. This study explains the shift of government control, highlights instances of pushback, and identifies limitations on the Kremlin's strategy going forward. The Kremlin's centralization drive has manifested in several ways, including tightening control over regional and municipal political institutions, expanding financial control over regional budgets and policy priorities, nationalizing and indirectly mobilizing business assets, and introducing new priorities in personnel policy. These changes have created winners and losers, resulting in friction and resistance from regional elites who perceive their interests and autonomy as threatened. The sustainability of the Kremlin's strategy is uncertain and risks intensifying tensions and worsening government instability.

Lessons from Minsk II for the Ukraine peace talks Brussels Signal

The road to peace in Ukraine is extremely difficult and perhaps also very long, despite President Trump’s initial hopes. Even agreeing an initial ceasefire in Ukraine is a tall order, as this Tuesday’s Trump-Putin phone call attests. Nonetheless, negotiations will continue, particularly as all sides – Ukraine, Russia and the US – appear committed to achieving a full peace agreement rather than merely a Korean-style ceasefire. Yet a full peace treaty is much more considerable undertaking, and these negotiations remain overshadowed by the failure of the Minsk II Agreement – a 2015 diplomatic effort that promised peace but ultimately collapsed. The lessons of Minsk II offer sobering insights into the obstacles facing any new settlement and the structural flaws that must be avoided if a sustainable resolution is to be achieved.

Russia’s Peace Demands on Ukraine Have Not Budged Council on Foreign Relations

President Trump, in his recent address to Congress, said Russia has sent “strong signals that they are ready for peace.” Is that true? Not really. The Kremlin has not budged from its maximal demands for ending the conflict, which Russian President Vladimir Putin laid out last June and includes:

No NATO membership for Ukraine;

Ukraine’s recognition of Russia’s annexation of four Ukrainian provinces (even though Russia does not physically control all the territory of three of them);

Ukraine’s demilitarization and denazification (code for the installation of a pro-Russia puppet in Kyiv); and

the lifting of anti-Russia sanctions.

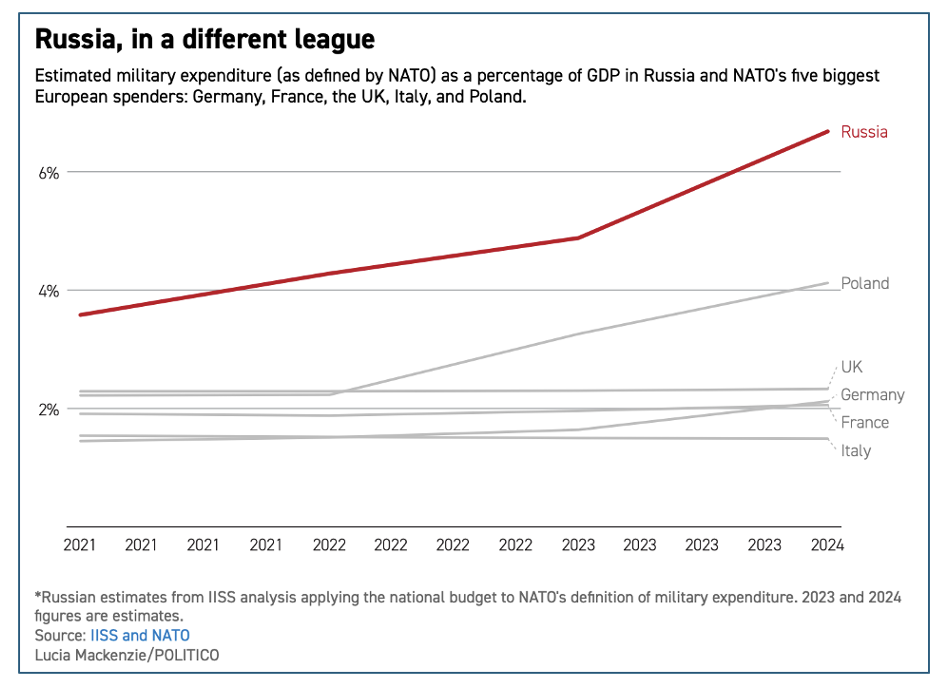

During a visit to the Defenders of the Fatherland Foundation, Putin doubled down on that position just last week, saying that Russia does not intend to make any compromises in peace negotiations. The Russian president sees no need to make any concessions. His armies are making grinding progress on the battlefield, albeit at a heavy cost in men and materiel. The Russian economy has proven resilient to Western sanctions, growing by more than 4 percent each of the past two years. Ukraine, meanwhile, is facing severe manpower shortages, and Western support is flagging.

Turkey in a Trump-and-Putin World Carnegie Endowment for International Peace

The disruptions to the world order caused by Russia and the new U.S. administration complicate Turkey’s balancing act between Moscow and the West. But these shifts could offer Ankara a chance to shape the evolving security dynamics and contribute to Europe’s stability. Yet Turkish President Recep Tayyip Erdoğan cracked down on Turkish opposition parties this past week, arresting dozens of politicians, fearful of losing power in the upcoming elections and exposing the fragility of his government.

A Blueprint for a European Defense Force Strategic Europe

As the U.S. commitment to Europe’s security wanes and Russia’s threat to the continent grows, the need for a European defense force is becoming more pressing than ever. By expanding existing frameworks and investing in Ukraine’s defense industry, Europe can begin to take charge of its own security.

The Tariff Wars

The Incoherent Case for Tariffs Chad Brown/Douglas Irwin – Foreign Affairs Magazine

Less than two months into his second term, U.S. President Donald Trump has made good—with startling intensity—on his campaign promise to impose tariffs. On inauguration day, he issued the America First Trade Policy Memorandum to review U.S. trade policy with an eye toward a new tariff regime. Over the first two weeks of February, he set in motion new duties covering nearly half a trillion dollars of U.S. imports. On March 4, he doubled the size of his already significant February tariff increase on China. Over this period, he has also announced, suspended, announced again, and suspended again 25 percent tariffs on goods from Canada and Mexico. And his administration has pledged to impose reciprocal tariffs on April 2. The result has been uncertainty, chaos, and immediate retaliation from some of the United States’ biggest trade partners. All this economic upheaval raises a central question: Why is Trump so focused on tariffs?

Trump’s tariffs challenge India’s economic balance The Australian Strategic Policy Institute

US President Donald Trump’s tariff threats have dominated headlines in India in recent weeks. Earlier this month, Trump announced that his reciprocal tariffs—matching other countries’ tariffs on American goods—will go into effect on 2 April, causing Indian exporters to panic at the prospect of being embroiled in Trump’s escalating trade war. The economic impact on India, which runs a trade surplus with the US, could be significant. India exported goods worth nearly $74 billion to the US in 2024, and estimates suggest that Trump’s new tariffs could cost the country up to $7 billion annually. But the implications could be much more far-reaching. One analysis estimates that India effectively imposes a 9.5 percent tariff on US goods, while US levies on Indian imports are only 3 percent. If Trump follows through on his pledge of full tariff reciprocity, that imbalance will vanish—along with the cost advantages many Indian exporters currently enjoy.

Antitrust Fuels Trade Tensions CEPA

President Donald Trump’s tariff threats target “discrimination against American innovation,” and US legislators point to the EU’s Digital Markets Act as evidence – even as the US pursues its own tech antitrust cases. The tensions underline a troubling reality: antitrust enforcement has become politicized, and as the Paris-based OECD Club of advanced democracies has long recognized, the politicization of antitrust enforcement makes markets less dynamic, less competitive, and less efficient, ultimately harming consumers. This outcome can be avoided if both European and American leaders depoliticize and focus enforcement on making markets work for consumers.

The Optimal Monetary Policy Response to Tariffs Javier Bianchi & Louphou Coulibaly/NBER

What is the optimal monetary policy response to tariffs? This paper explores this question within an open-economy New Keynesian model and shows that the optimal monetary policy response is expansionary, with inflation rising above and beyond the direct effects of tariffs. This result holds regardless of whether tariffs apply to consumption goods or intermediate inputs, whether the shock is temporary or permanent, and whether tariffs address other distortions.

Geoeconomics

Should Friday be the New Saturday? Hours Worked and Hours Wanted National Bureau of Economic Research

This paper investigates self-reported wedges between how much people work and how much they want to work at their current wage. More than two-thirds of full-time workers in German survey data are overworked—actual hours exceed desired hours. We combine this evidence with a simple labor supply model to assess the welfare consequences of tighter weekly hours limits via willingness-to-pay calculations. According to counterfactuals, the optimal length of the workweek in Germany is 37 hours. Introducing such a cap would raise welfare by .8-1.6% of GDP. The gains from a shortened workweek are largest for workers who are married, female, white collar, middle-aged, and high-income. An extended analysis integrates a non-constant wage-hours relationship, falling capital returns, and a shrinking tax base.

Around 60% of the fixed-rate debt in the OECD that will mature by 2027 (approximately $9T) was issued in 2021 or earlier, before the recent tightening cycle, most likely at yields below current market rates. The weighted average YTM of the maturing debt in 2025-27 remains below 2% in all three years, [while] the average of the projected 10-year interest rate in OECD countries is expected to remain around 3.6% in 2025. The debt maturing in 2025-27 will, therefore, likely be refinanced at nearly twice the original rates. Increased borrowing needs and high borrowing costs have driven interest payments to a higher share of GDP in 2024, [contributing to] the first increase in the central government marketable debt-to-GDP ratio since 2020. The supply of bonds needing to be absorbed by the market accelerated as central banks continued to scale back their holdings. Four countries — France, Spain, the United Kingdom, and the United States — face heightened vulnerability, with the debt maturing by 2027 exceeding 15% of their current GDP and the average yield-to-maturity on debt issued in 2024 surpassing that of this maturing debt by over 1.5 percentage points.

Africa and Critical Minerals

·Zimbabwe’s lithium beneficiation policy: a catalyst for Vision 2030 ISS/Africa Futures

As the global green energy transition gains momentum, lithium has emerged as the new gold, particularly in the automotive industry, due to its essential role in lithium-ion batteries. The demand for lithium continues to soar, and Zimbabwe stands at a competitive advantage as home to Africa’s largest lithium reserves and ranking among the world's top five in estimated deposits. If managed effectively, lithium beneficiation can drive Zimbabwe towards achieving its Vision 2030, transforming the country into an upper-middle-income economy. A fundamental aspect of this ambitious goal is attaining a GDP growth rate of 8–9% by 2030.

Can the DRC Leverage U.S.-China Competition Over Critical Minerals for Peace? Carnegie Endowment for International Peace

The Democratic Republic of the Congo (DRC) is offering the United States access to its mineral resources in an effort to ensure peace and stability in the country. The offer, made against the backdrop of U.S.-China competition over critical minerals, is designed to motivate Washington to play a decisive role in the security crisis in the eastern DRC. Unlike in 2012, when then-president Barack Obama threw his weight into pressuring Rwanda to halt its support for the M23 (March 23) rebel movement, more recent U.S. administrations, past and current, have struggled to play a decisive role in the conflict raging in the eastern DRC, where the Congolese government is battling Rwandan-backed M23/AFC (Alliance Fleuve Congo) rebels.

Latin America

Chevron Out, Black Market In? The Fallout of U.S. Sanctions on Venezuela Oilprice.com

On February 26, President Trump announced his intention to end General License 41, which allowed Chevron to operate in Venezuela despite sanctions. The U.S. Treasury’s Office of Foreign Assets Control (OFAC) had created a system to monitor at least part of Venezuela’s oil industry by waiving sanctions for certain American, European, and Indian companies but with strict limitations. Four corporations that were authorized by licenses or comfort letters—Chevron, Repsol, Maurel et Prom, and Eni—contributed to a production of 325,000 barrels per day (bpd) in January, to the country’s total of 1,068,000 bpd, according to PDVSA, the state-owned energy company. The big question now is will it spur a massive rise of black-market oil coming out of Venezuela?

A Key Pending Challenge for Milei’s Argentina Americas Quarterly

Argentine President Javier Milei campaigned on two key promises: To bring the country’s high and accelerating inflation to a halt by dollarizing the economy and closing down the Argentine central bank (BCRA) and to balance the budget by taking a chainsaw to wasteful government spending. Now, 15 months into his term in office, he has made heroic progress on the fiscal and inflation fronts. But by forsaking dollarization and keeping currency and capital controls in place, Milei has jeopardized his anti-inflationary program and discouraged a potential investment boom.

North Korea

The North Korean tourist trap The interpreter/Lowry Institute

Having closed the country even more tightly during the Covid pandemic, last month, North Korea put out the welcome sign for a small group of foreign tourists from Australia, the United Kingdom, France, Germany, and Canada for the first time since 2020. Yet the gates slammed shut again last week when Pyongyang announced it would grant no new tourism visas. Visitors from Russia have been allowed in since February 2024, but Chinese nationals, once North Korea’s main source of foreign tourists, have still not returned. The abrupt closure raised eyebrows, considering that North Korea’s Kim Jong-un has invested in key tourism facilities in Mount Chilbo, Mount Paektu, Mount Kumgang, and the Wonsan-Kalma resort area in preparation for the post-lockdown rebound in foreign visitors.