Fulcrum Perspectives

An interactive blog sharing the Fulcrum team's policy updates and analysis.

Recommended Weekend Reads

June 12 - 14, 2026

The Battle Over Data Centers, Is the iPhone Birth Control?, Germany’s Evolving Defense Policy, and US Debt Levels Won’t Be Sustainable in 20 Years

Below are a number of studies, research reports, and news analyses we read this past week. We thought you might find them of interest and, hopefully, of use. Please let us know if you have any questions.

The Growth and Growing Battle Over Data Centers

Latin America’s Data Center Gold Rush: Myth and Reality Americas Quarterly

The numbers speak for themselves: Google is building an $850 million data center in Uruguay; Amazon committed $5 billion to a new cloud region in Mexico; and Microsoft is investing $2.7 billion in cloud and AI infrastructure in Brazil. From Montevideo to Querétaro, data center providers are expanding capacity, governments are rolling out tax incentives, and multilateral banks are publishing frameworks to help countries “capture the data center opportunity.” The opportunity is real. So is the risk of misreading it. Latin America and the Caribbean are emerging as credible destinations for digital infrastructure investment for reasons that go beyond hype. The region’s electricity matrix is a structural asset: Brazil generates nearly 90% of its electricity from renewables, and companies like Equinix, Ascenty and Scala have expanded aggressively in São Paulo for exactly that reason.

OpenAI’s Threat Report: “Data Center Bandwagon” The Special Competitive Studies Project

In this YouTube interview, OpenAI’s Ben Nimmo, who leads the company’s intelligence and investigations work, details a covert influence operation — likely out of China — that used ChatGPT to generate content posted by fake accounts posing as Americans, aimed at one surprising target: America’s own data centers. Ben connects it to a pattern that should worry anyone tracking the AI race, and answers the question— why reach for ChatGPT instead of China’s own DeepSeek?

America’s Data-Center Build-Out Is Falling Way Behind Schedule Wall Street Journal

Tech companies are earmarking unprecedented sums of money to finance the build-out of massive data centers, with a planned $85 billion equity-raise by Google being the latest example. But even as the piles of capital secured have grown ever larger, the ability to deploy it in the artificial-intelligence race has become less certain. Supply-chain backlogs, permitting fights and availability of power supplies are among the issues that have caused the construction of data centers to fall behind targeted timelines, with the gap growing wider in recent months: A JPMorgan analysis last month found that more than 60% of data-center capacity planned for completion in 2027 isn’t yet under construction, and another 7% is delayed. It is a seeming paradox: If hyperscalers can’t break ground on many of the projects they have already announced, what difference can hundreds of billions of dollars more make—however eager Wall Street may be to supply it?

Demographics

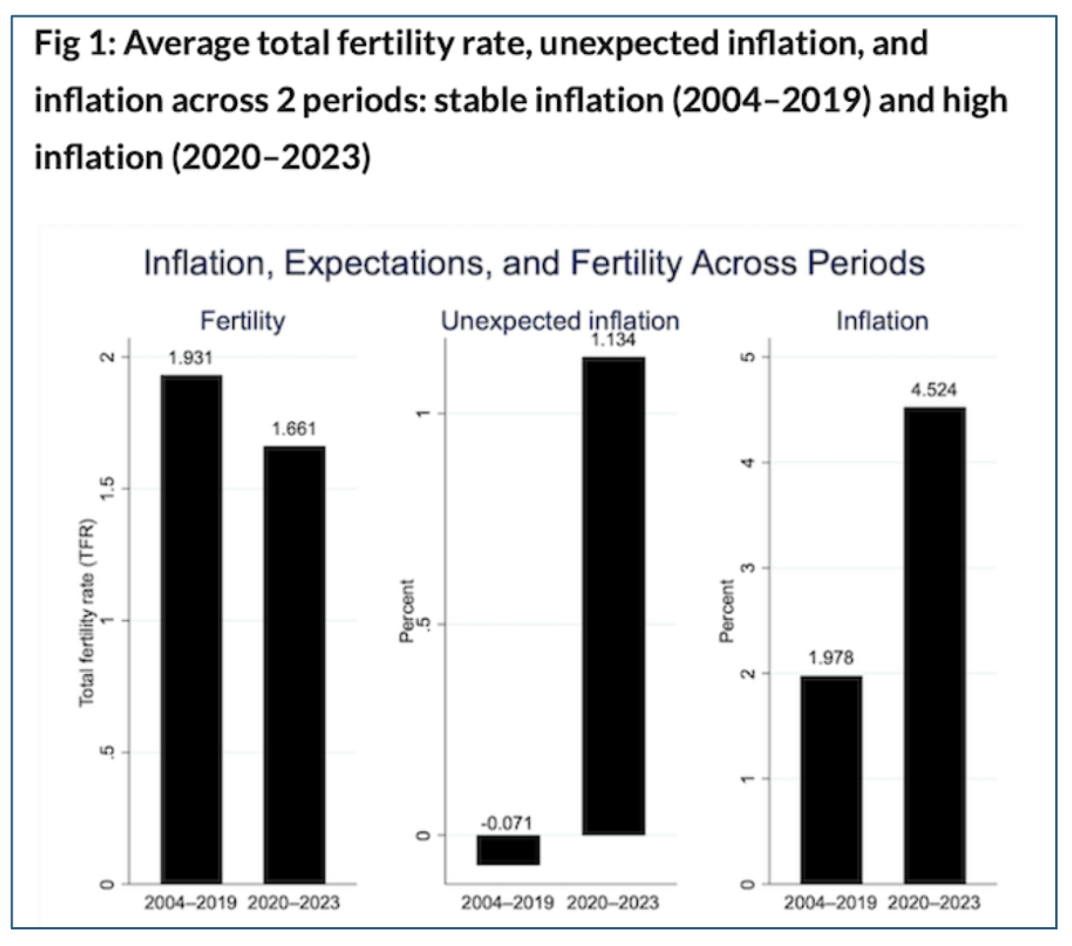

·Is the iPhone Birth Control? Causal Evidence from AT&T’s 2007–2011 Carrier Monopoly Caitlin Myers & Ezekiel Hooper/National Bureau of Economic Research

Abstract: The U.S. general fertility rate has fallen by 22% since 2007, a sustained decline not readily explained by economic conditions, contraceptive use, housing or childcare costs, or other commonly cited factors. We assess the potential role of a different shock: the diffusion of the smartphone. The U.S. rollout of the iPhone, the first modern smartphone, provides a natural experiment: from June 2007 through February 2011, the device was sold only on AT&T, allowing us to identify its effect from variation in AT&T’s mobile broadband coverage. Entropy-balanced Poisson and synthetic difference-in-differences event studies imply that access to the iPhone reduced births by 4.5–8.0% at ages 15–19 and 3.2–6.6% at ages 20–24, with statistically significant but smaller declines among older cohorts. Placebo analyses applied to Verizon and Sprint’s pre-2011 coverage footprint are null. Taken together, these cohort effects imply that the diffusion of the iPhone deepened the decline in births among women under 30 while suppressing the rise in births among older women. Overall, the diffusion of the iPhone explains 33–52% of the decline in the general fertility rate among women aged 15–44. National-survey evidence on time use and sexual behavior is consistent with the iPhone reducing in-person interactions, increasing pornography use, and reducing sexual frequency.

India’s population will soon be falling—probably quite fast The Economist

In 1950 India’s population was 360m. The average woman had six children—roughly the same as an American woman a century earlier. Today, with a population of 1.45bn, India accounts for a sixth of humanity. It surpassed China as the world’s most populous country in 2023 and has kept growing. But its total fertility rate (tfr), the number of births a typical woman has over her lifetime, has fallen to 1.9 (see chart 1), below the level needed to keep the population stable in the long run. Although the population will keep growing for a spell, as the generation that are currently children themselves become parents, a future contraction is inevitable unless the fertility rate rises back above 2.15. In practice, it is likely to keep falling, accelerating the impending shrinkage. In Delhi, for instance, the tfr is 1.2.

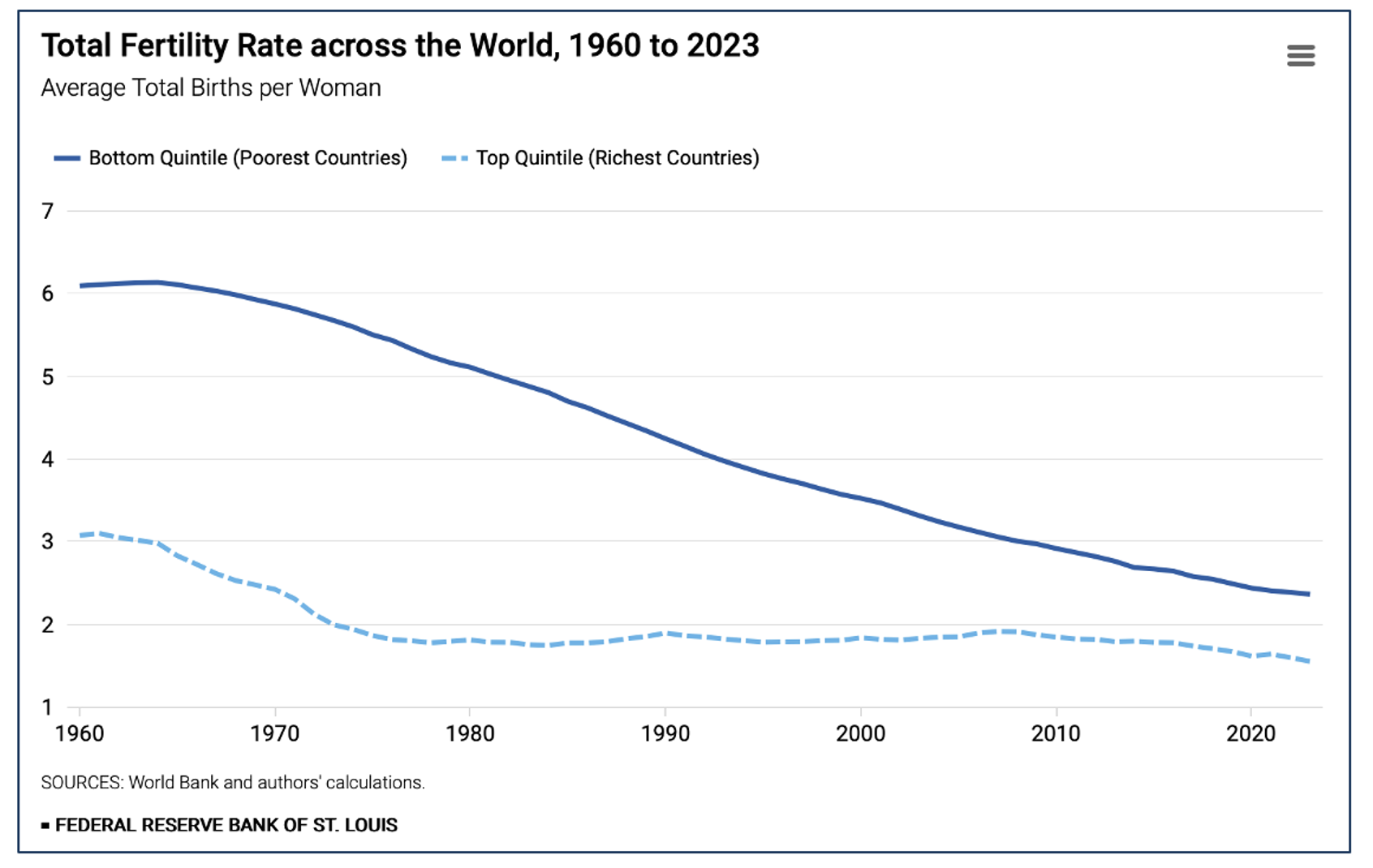

Declining Fertility Rates Across the World Federal Reserve Bank of St. Louis

The total fertility rate (TFR), or the average number of births per woman over her entire reproductive life, is one factor affecting population growth. Trends in the TFR have implications for the world’s demography. Although poor countries have a higher TFR than rich countries, the rate has been declining in both for 60 years. This has narrowed the TFR gap between the poorest and richest countries from three children per woman to less than one child per woman. In rich countries, the TFR has been lower than the rate needed to maintain population levels for a few decades. But the TFR in low-income countries remains higher than the replacement rate.

Europe’s Evolving Defense Strategy: The German Perspective

Understanding Germany's Defense Strategy Chain Reaction Podcast/Foreign Policy Research Institute

The podcast features a conversation with FPRI President Aaron Stein and Roderich Kiesewetter, a Member of the German Bundestag (CDU/CSU) who has held various command and staff positions, including at the EU Council , NATO and the German Ministry of Defense. The two discuss the strategic framework of the recently released German defense policy, key reforms and capabilities, and what strength means in the new European security environment.

Making Defense European Again European Council on Foreign Relations

Between an expansionist Russia and a careless America, one thing is clear: Europeans must be prepared to defend themselves, and quickly. To do so, they need to adopt a distinctly European way of defense. They cannot hope to replicate America’s security approach, nor do they need a new institutional superstructure. Rather, they need to be pragmatic and resourceful by building on what exists. A European way of defense has three pillars. First, a layered decision-making architecture would draw on NATO’s command structure for military operations; on the EU for funding and pan-European solidarity; and on minilateral arrangements for fast adaptability. Second, Europeans would build up their military capabilities, capacity and readiness to deter and defend effectively with little to no American help. Third, all of this must rest on a coordinated European defense industry wherever possible and draw on capabilities from diversified, allied sources if needed. This model would set Europeans up to defend themselves with America where possible, with less America where necessary and without America if it comes to that.

The Overall Concept of Military Defense: Military Strategy and Plan for the Armed Forces German Federal Minister of Defense

The German Ministry of Defense recently published its first-ever integrated military strategy connecting threat assessment to force structure to capability investment over a defined timeline — the most serious attempt in the history of the Federal Republic to close the gap between strategic understanding and actual defense commitment. The plan runs in three phases: a rapid buildup through 2029, a capability-focused expansion through 2035, and a longer-term technology-driven phase through 2039 and beyond. Together with its allies, Germany aims to be ready to deploy at least 460,000 troops to deter potential aggression.

The U.S. Federal Debt

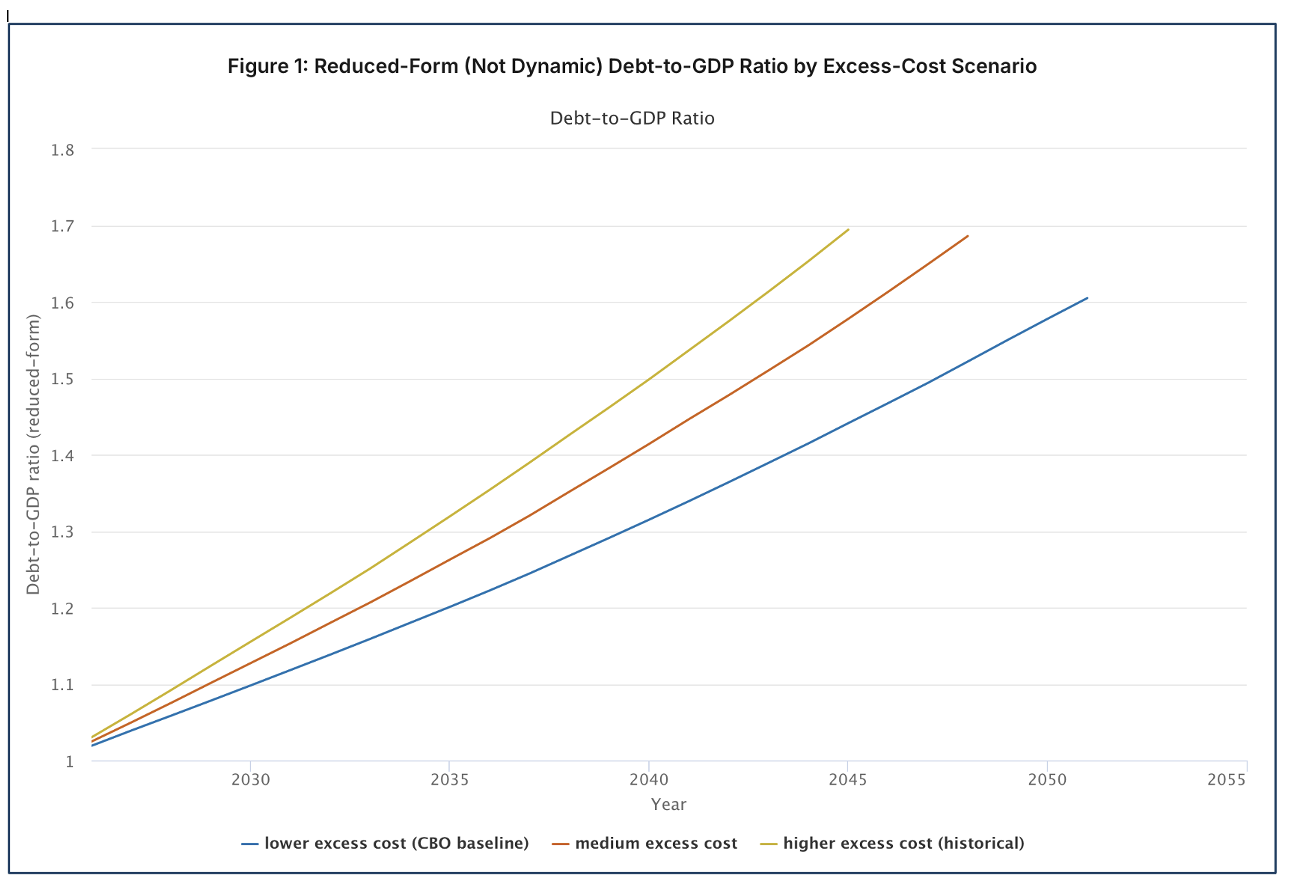

When Does Federal Debt Reach Unsustainable Levels? Spring 2026 – Onward Penn Wharton Budget Model

The Penn Wharton center estimates that the United States federal debt cannot rationally exceed roughly 210 percent of GDP as an outer limit. Under historical excess cost growth in healthcare, this outer limit is likely reached within 20 years; there is a 25% chance of reaching it in 14 years. Debt markets unravel earlier if beliefs about government repayment shift.

Recommended Weekend Reads

June 5 - 7, 2026

Assessing U.S. Military Options Toward Cuba, Chile’s Investment Reset, China Considers the Challenge of Ruling Taiwan, and Is AI Creating Value?

Below are a number of reports and articles we read this past week and found particularly interesting. Hopefully, you will find them both interesting and useful. Have a great weekend.

Americas

The Next Caribbean Crisis? Assessing U.S. Military Options Toward Cuba Center for Strategic & International Studies

The United States has engaged in touch-and-go negotiations with various figures within the Cuban communist regime, while at the same time issuing an executive order to further increase economic pressure on the island. The United States has stepped up military surveillance overflights of Cuba, gathering intelligence on the capabilities and dispositions of the country’s Revolutionary Armed Forces (FAR). In late May, CIA Director John Ratcliffe met with Cuban leaders, bringing along a paramilitary officer who was involved in capturing Maduro and killing the Cuban military personnel who were guarding the Venezuelan leader. It was a sign of what could come if negotiations are unsuccessful. Although the crisis in the Persian Gulf continues to smolder, the United States has enough military assets to operate simultaneously in the Western Hemisphere. While the ultimate objective of U.S. Cuba policy remains unclear, the possibility of military action is present. Therefore, it is worthwhile to examine a range of possible scenarios involving the use of force against Cuba. This report examines five such scenarios, their relative likelihoods, and the risks involved.

Why Brazil–U.S. Relations Will Worsen Before They Improve Latin America Takeaways

Between new tariffs on Brazil and the recent announcement of new U.S. measures targeting Brazil criminal gangs— the designation of the PCC and Comando Vermelho as terrorist organizations and, more recently, the conclusion of the Section 301 investigation — domestic political analysis has focused more on the electoral implications of these developments than on their broader consequences for the overall trajectory of the bilateral relationship. As the Brazilian elections get closer, the U.S.-Brazil relationship is likely to worsen before getting better.

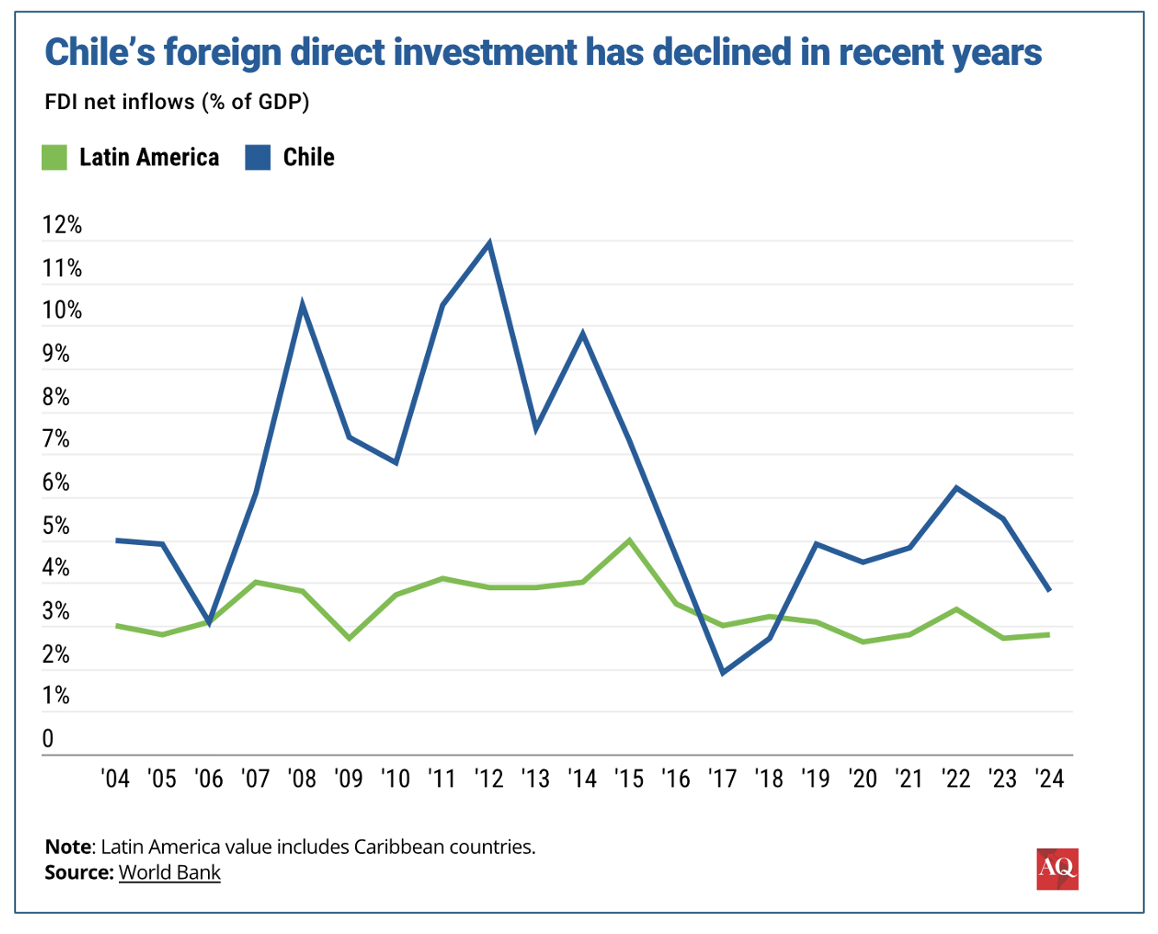

Kast and Chile’s Investment Reset Americas Quarterly

For decades, Chile stood out as Latin America’s most reliable destination for foreign direct investment (FDI), capturing as much as $192 billion between 2000 and 2014, or 7.4% of the region’s total net inflows. But since then, the country has endured a substantial erosion of its ability to attract international capital. That may be about to change. In April, President José Antonio Kast submitted an economic reform to Congress — the Reconstruction and Economic Development (RED) bill — that seeks to modernize the investment regime and encourage both international and local investment as the government aims to boost GDP growth to 4% annually by the end of his administration, double the average annual GDP growth rate reported since 2014. The goal is to reset the investment climate after years of lackluster performance, and the House already passed the proposal, which the Senate will begin discussing today. Kast defended the scope of the reform during his first annual address to the nation held at the National Congress in Valparaiso on Monday. Reviving the investment environment and redefining its institutional framework presents a challenge: how to rebuild economic dynamism without undermining the regulatory legitimacy gained through social and political reforms of the recent past. This is a political question, not only an economic dilemma.

U.S. Foreign Policy in the Western Hemisphere: Issues for Congress Congressional Research Service

The Congressional Research Service – the research arm of the U.S. Congress – recently prepared an updated brief for members of Congress on the region and official U.S. policy. It offers a good high-level overview of all that has changed in U.S. foreign policy for the region.

Delcy Rodríguez Tries to Show She Has a Debt Strategy Caracas Chronicles

In April 2026, the IMF and World Bank resumed dealings with Venezuela for the first time since 2019, opening the path to a formal economic assessment and potentially unlocking $4.9 billion in frozen special drawing rights. In May, the Delcy administration announced a “comprehensive restructuring of its sovereign debt” and PDVSA obligations, appointing Centerview Partners as financial adviser and pledging a macroeconomic framework by June. This did not include a request for a macroeconomic program established by the Fund, which distanced itself from Venezuela’s announcement shortly after. According to Reuters, Venezuela’s total liabilities could be above $150 billion. On June 2, Venezuela added Hogan Lovells as legal counsel for the restructuring under a dual mandate that also covers strategic lobbying for the Venezuelan embassy in Washington. The account is led by Norm Coleman, a former Republican senator with deep political connections in the capital. Neither selection has been free of political entanglement. Former Trump official Mauricio Claver-Carone, earmarked by The Washington Post as Venezuela’s unofficial viceroy, has vouched for Centerview. His business partner, Jessica Bedoya, was on the same chartered flight to Caracas as two Centerview executives on February 12, weeks before the firm finalized its contract (Centerview denied Bedoya played any role in their assignment).

The US plan for Venezuela won’t work without the rule of law. Here’s how to make progress Chatham House

Drawing on discussions with a group of experts including Venezuelan and international jurists, diplomats, scholars of democratic transitions and democratization, and representatives of the Venezuelan opposition, this policy paper sets out recommendations for incremental, integrated steps to achieving rule-of-law reform in post-Maduro Venezuela. The paper makes the case that a negotiation and monitoring process must be put in place without delay, with the committed involvement of the US, the interim Venezuelan government, multilateral organizations, diplomatic missions, investors, and local business and civil society. The framework for this process will need to identify priorities, benchmarks, and a timeline for institutional and legal reforms, and it should clearly articulate how judicial, commercial, legal, and human rights reforms relate to, and underpin, economic and political development.

Indo-Pacific

How China Misperceives Itself Foreign Affairs

Great powers rarely fail because they are unaware of their problems. More often, they fall apart because they misidentify or only partially identify the root of those problems. The ability to accurately diagnose weaknesses, to distinguish between temporary constraints and structural limits, and to generate the political will to fix deep-seated problems separates states that adapt and thrive from those that stagnate or crumble. China today faces an imposing list of challenges that it needs to assess and address. Economic growth is slowing, the population is aging, the financial system is under stress, and other countries have been tightening trade controls and scaling up their own industrial policies to compete. For many years, China’s economic expansion could mask the country’s underlying vulnerabilities. That era is now over. And in party documents and major speeches alike, leaders in Beijing admit these pressures and acknowledge the country’s weaknesses.

After the Invasion: China Considers the Problem of Ruling Taiwan War on the Rocks

In August 2024, scholars at a Xiamen-based think tank published a paper urging Beijing to immediately establish a shadow Taiwan government on the Chinese mainland in preparation for a full takeover of the island. “It is imperative to prepare a plan for the comprehensive takeover of Taiwan after unification,” they said. The scholars were writing at a fraught moment for Beijing. Only months earlier, the anti-China Democratic Progressive Party had taken office after a third consecutive presidential election win. Unusually for a Chinese publication on such a sensitive topic, the paper made several frank admissions: that opposition to unification within Taiwan had deepened rather than softened; that Hong Kong’s post-1997 governance model was ill-suited to Taiwan; and that many Chinese officials lacked even a basic understanding of political and social conditions on the island. The paper circulated briefly before disappearing from China’s internet, which underscored the sensitivity of the topic and the rarity of such candor.

The Iran Effect: Showing The Many Challenges to Crude Oil Processing

The global refining disorder: The political geography of crude processing Alexander Etkind, Georg-Kaup, Ayansina Ayanlade, Gustavo Andreao/Energy Research & Social Science

Abstract: Why are refineries where they are, and what forces explain their distribution across planetary space? This article develops the concept of the Global Refining Disorder (GRD) to analyze the political geography of crude oil processing. Departing from location theory, which privileges transport-cost minimization, we argue that refinery siting is determined by the interplay of national strategies, security regimes, postcolonial legacies, and economies of scale. We identify two ideal types of refining political economy — the mercantile pump, which concentrates processing capacity near centers of power and imports crude from peripheries, and the developmental syringe, which locates refining near extraction sites to stimulate peripheral growth. Working across five comparative cases – the United States, Russia, Saudi Arabia, Brazil, and Nigeria – we analyze the transportation triangles shaped by oil fields, refineries, and consumers of fuel. To operationalize these carbon flows, we calculate two derived measures — refining lag and the export-to-refining ratio. With the concept of securitization of scalability, we explain how economies of scale generate systemic vulnerability of refineries. Recent events in Ukraine and Iran empirically demonstrate that refineries constitute the most vulnerable component of the global energy system. Looking forward, we argue that the path from refining to circularity secures decentralization of energy supply, with political choice — rather than geological endowment or market signals — remaining the decisive variable in transition.

Is AI Creating Value?

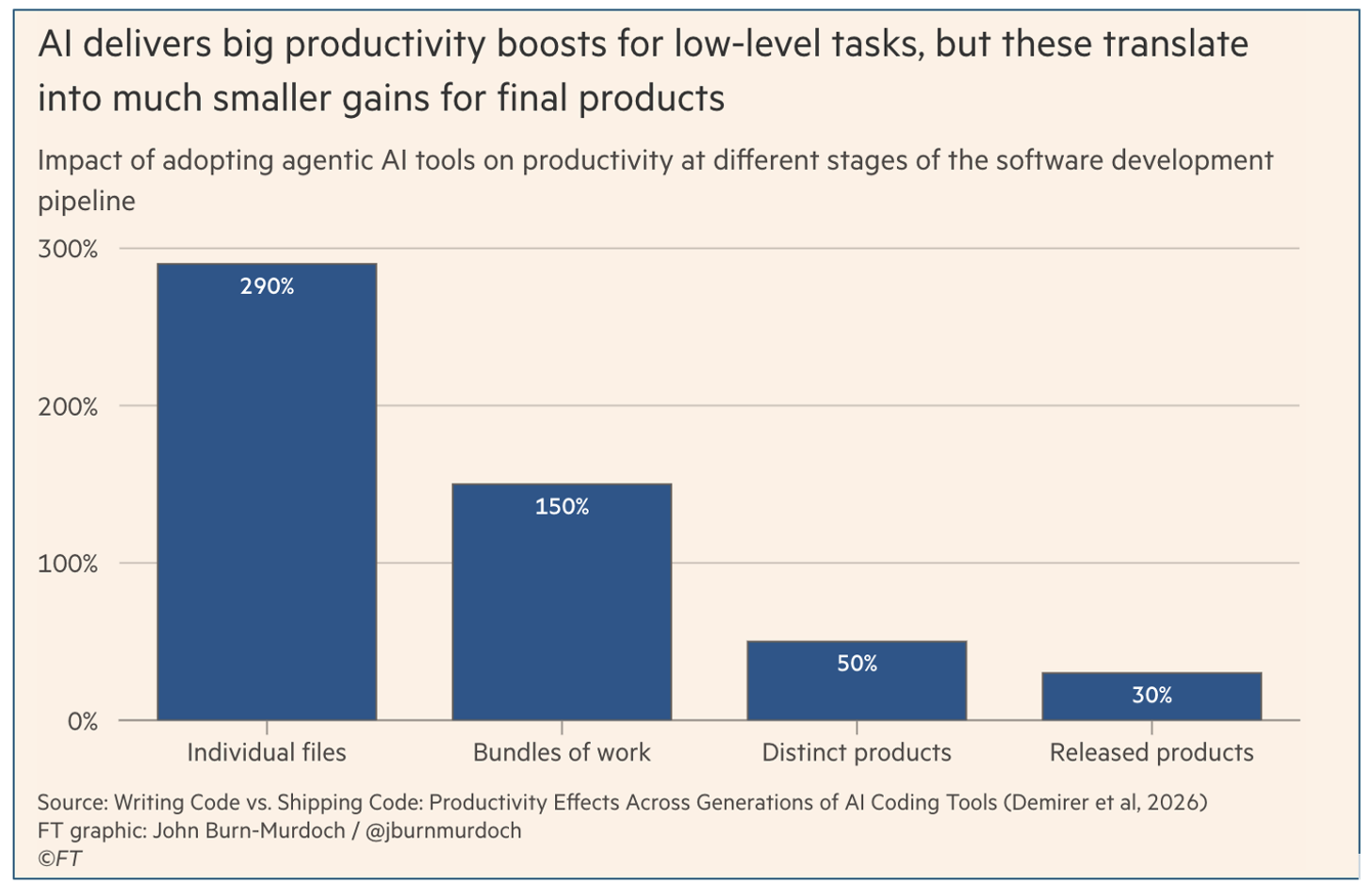

Writing Code vs. Shipping Code: Productivity Effects Across Generations of AI Coding Tools Mert Demirer, Leon Musolff & Liyuan Yang/National Bureau of Economic Research

The Financial Times Data Points columnist John Burn-Murdoch wrote an intriguing piece asking if AI was really creating much value. Burn-Murdoch wrote, “One particular point of tension between AI’s boosters and detractors has been the disconnect between reported increases in coders’ output and the apparent lack of a corresponding boom in product or value creation. A new paper leaves both sides able to claim vindication. The study by MIT’s Mert Demirer and co-authors tracked software developers’ work before and after they adopted AI tools. Importantly, they measured this at several different levels, from the amount of code written, to the number of discrete files edited, to the number of projects or features worked on, to actual releases of new software. They found an explosive impact at the top of this funnel — coders created or edited almost 300 per cent more files — but that boost was halved to 150 per cent by the time they got to the number of discrete pieces of work submitted for review, and that in turn shrunk fivefold to a roughly 30 percent uplift in the number of full software releases. This is the study. And here is the abstract:

Abstract: How do the productivity effects of AI evolve across successive generations of tools, and to what extent do task-level gains ultimately translate into final output? We study these questions in the context of software development, using data on more than 100,000 GitHub developers combined with their AI usage telemetry. In a matched event study design, we find that autocomplete, interactive coding agents, and autonomous coding agents each significantly increase coding activity (“commits”), with respective cumulative effects of 40%, 140%, and 180%. These gains, however, attenuate sharply across the production hierarchy: the 180% cumulative effect falls to 50% for the number of projects, and to 30% for actual releases. This pattern is consistent with the weak-link hypothesis: the strong productivity gains from AI are attenuated by human bottlenecks in the production chain, with an estimated elasticity of substitution of 0.25 between AI and human effort, which indicates strong complementarities. We further confirm these results across four major app marketplaces, finding a moderate increase in the number of new apps but no increase in total usage. Large task-level AI productivity gains have therefore translated only partially into shipped and used software thus far.

Recommended Weekend Reads

May 29 - 31, 2026

Below are a number of reports and articles we read this past week and found particularly interesting. Hopefully, you will find them of interest and useful as well. Have a great weekend.

Sanctions, Tariffs, and the Financing of Global Wars

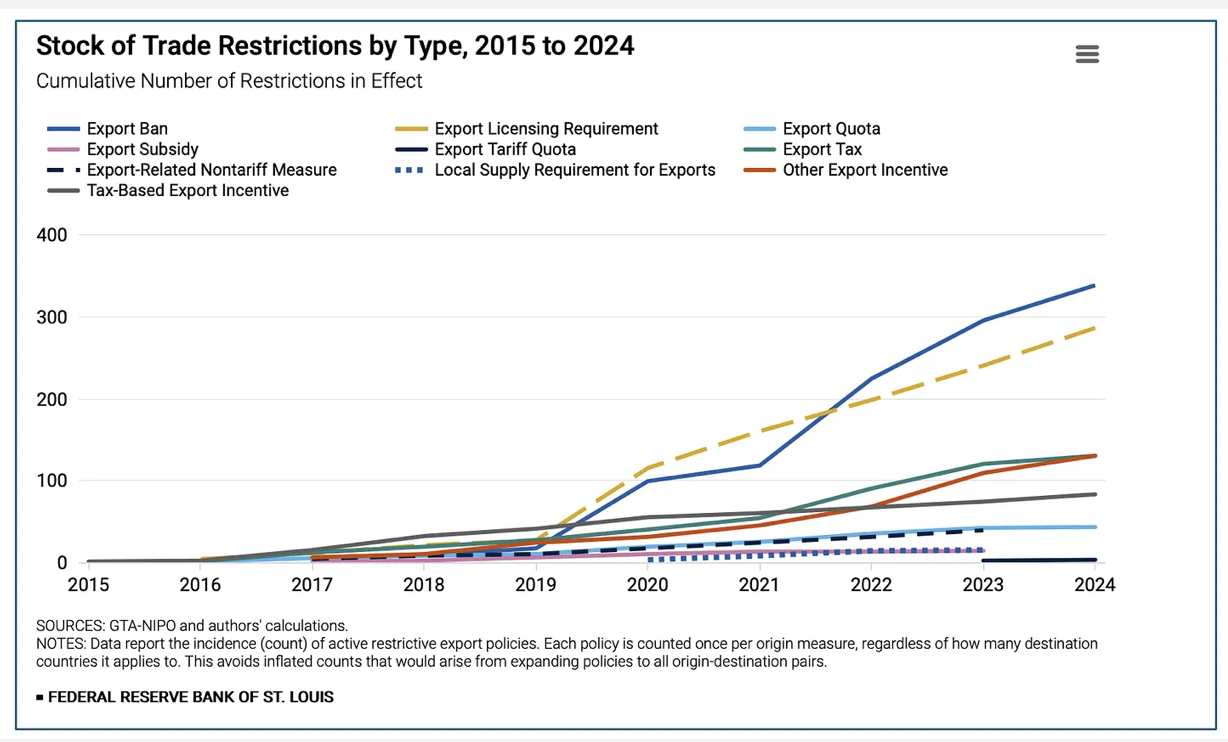

How Trade Policy is Changing: From Broad Rules to Targeted RestrictionsFederal Reserve Bank of St. Louis

From 2015 to 2024, the number of new export-related trade restrictions introduced across the globe each year and the cumulative number of restrictions in place both grew, with a particularly sharp increase after 2019.During this period, trade restrictions accumulated steadily across a wide range of policy instruments, reflecting a sustained shift in how trade policy is used.Targeted measures, particularly export bans and licensing requirements, expanded much faster than traditional, broad-based trade instruments like tariffs.The effects of targeted trade restrictions are not spread evenly across the global economy; rather, they tend to be concentrated in certain strategic, high-value and high-technology sectors.

States as Financiers: International Lending in War and Peace Kiel Institut

States are major international financiers, but their role is poorly understood. We study state-driven cross-border lending over two centuries using a new database covering 1.2 million official loans and grants by 134 governments and 70 multilateral institutions since 1790. We document a dual, state-contingent structure of international credit. In normal times, private creditors dominate cross-border lending. In adverse states of the world, such as wars and financial crises, official creditors step in, at times on a massive scale. These official flows are driven by great powers, are highly subsidized, and are largely absent from canonical models in international macroeconomics.

Perspectives is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

Shifting Conclusions From The Crises Of The Past 30 Years Louis-Vincent Gave Gavekal Research

Louis-Vincent Gave argues that “the lesson of the Strait of Hormuz” is to continue the shift toward investments in gold and industrial commodities – which will create a sustained liquidity drain on global financial markets. The lesson of the 1997-98 Asian and emerging market crisis was to accumulate more US treasuries. The lesson of the 2008 global mortgage crisis was to accumulate more US treasuries. The lesson of the 2011-13 eurozone crisis was to accumulate more US treasuries. The lesson of the 2022 Ukraine war and consequent financial sanctions was to accumulate more gold. Then what will be the lesson of the Strait of Hormuz crisis? Odds are it will be to accumulate larger inventories of industrial commodities, energy and food while reinvesting in the resilience of one’s own power grid. All of this will require capital and therefore act as a sustained liquidity drain on global financial markets for years to come.

Geoeconomics: What’s the Cost of Coercion in Global Trade? Federal Reserve Bank of Boston Podcast

When countries practice geoeconomics, they use their economic might to win concessions from other nations. Geoeconomics can include tools like industrial policy, tariffs, and embargoes. But some say these economic coercion tactics could reduce trust and cooperation among nations – and have critical impacts on global trade. Listen to the panel discussion with economists Douglas Irwin, Karen Dynan, and Caroline Freund and download the paper given by professor Jeffry Frieden at the Boston Fed’s 69th Economic Conference, “The U.S. Economy in a Changing Global Landscape.

State Dependence of Monetary Policy During Global Supply Chain Disruptions Jesus Fernández-Villaverde/National Bureau of Economic Research

Abstract: We study how global supply chain disruptions affect monetary policy transmission. Post-pandemic evidence indicates surging transportation costs, goods-market imbalances, and rising prices. We develop a model in which logistical bottlenecks (upstream slack coexisting with downstream shortages) steepen the aggregate supply curve. This convexity amplifies price responses to monetary policy while dampening output effects. Threshold VAR and Local Projection estimates are consistent with this mechanism: during disruptions, contractionary policy reduces prices more at smaller output cost, easing the stabilization trade-off.

Glass Jaw? The New Economic Fragility Recasting American Power War on the Rocks

A pair of children’s shoes is an odd place to look for the changing dynamics of American power. But stick with me because, after the past year, it is one of the clearest places to see them. Long before those shoes reach a store shelf, tariffs have raised the cost of materials, components, and importation. Oil touches nearly everything else: synthetic fabrics, foam, adhesives, packaging, and freight. When both shocks arrive together, companies cut margins, cut orders, cheapen materials, delay investment, and eventually pass the pain on to consumers. Now, multiply that across the economy, and you start to see the troubling scope of the strategic problems this is causing. The Trump Administration’s International Economic Powers Act tariffis and subsequent Section 122 tariffs have degraded the ability and agility of the U.S. economic system to absorb future shocks — critical parts of the systemic bedrock of American economic power. This is vital to understand because America’s economic power is not being hollowed out exclusively because of the Iran war and decreased energy supplies. In reality, the oil crisis is being layered on top of America’s new tariff-induced fragility, pushing America into a new economic cycle: one of higher prices and diminished capacity for American businesses to absorb and navigate global shocks to their supply chains. American businesses are already feeling this in real time. The shocks are still moving through the system and more will follow.

What Demographic Prediction Can and Cannot Achieve Samuele Lo Piano, Marta Kuc-Czarnecka, Roger Pielke, and Andrea Saltelli Social Science Research Network

Abstract: Simulation of the decision chain yielding projections of world population in 2050 that range from 6 to 14B suggests most of the variance in demographic forecasts arises not from parameter uncertainty or data randomness but from model choice. We explore demographic predictions by propagating all plausible choices that can be made during the analysis through the modelling process. This approach involves navigating the so-called ’garden of forking paths’—mimicking in silico what would happen if multiple investigators were to examine the same problem. For this, we now abandon [the Chinese government mathematician] Song Jian’s ‘historic’ model and turn to models currently in use: the Cohort-Component and UN WPP models, the Lee-Carter model and the Lotka-Volterra model. Note that in standard use, these tools are used in isolation, see e.g. the FAO’s How to Feed the World in 2050, resting on a single UN WPP population trajectory shielding the reader from the compounding effect of their uncertainty. Unsurprisingly, the exercise capturing the modelling of the modelling process for global population projections to 2050 and 2075 reveals distinct characteristics regarding the sensitivity and projection outcomes of the different models. Once abandoned the straitjacket of Song’s approach, uncertainty is free to manifest itself. The overall uncertainty distributions of the projected populations show a wide range of possible outcomes, reflecting the inherent uncertainties in demographic projections.

Americas

Hong Kong and the Shadow Fleet: How One City Helped Sustain Maduro’s Oil Trade China Strategic Risks Institute

Whatever one thinks of the US government’s unilateral actions toward Venezuela in recent months, there should be no confusion about what networks used to help sustain the regime. Maduro’s regime remained in power through repression, corruption, and the systematic plunder of state resources while ordinary Venezuelans paid the price. The vessels moving Venezuelan crude outside normal channels were part of that survival strategy. They were part of what is commonly called the shadow fleet, the loose and constantly shifting ecosystem of ageing tankers, opaque shell companies, false flags, ship-to-ship transfers, and other deceptive practices used to move sanctioned oil for regimes such as Russia, Iran, and Venezuela. The usual way of telling this story is as a maritime one, about suspicious voyages, evasive maneuvers, and interdictions at sea. But the more important story is often on land. Again and again, when the ownership and management chains behind these vessels are traced backwards, they lead to Hong Kong, to shell companies incorporated there, to secretarial firms that provide them a sheen of legitimacy, and to a Western sanctions designation and enforcement system that fails to identify targets hidden in plain sight.

Cuba’s Only Choice: A Deal With Washington Is the Island’s Best HopeForeign Affairs

Ever since U.S. commandos removed Venezuelan President Nicolás Maduro from power in January, Washington has piled unprecedented pressure on Cuba, Caracas’s beleaguered former ally. The island’s economy had already been spiraling as a result of the first Trump administration’s “maximum pressure” sanctions, the COVID-19 pandemic, and Havana’s failure to adopt deeper economic reforms. But Cuba’s loss of access to heavily discounted Venezuelan oil dealt a lethal blow. Time is running short. Frustrated by Havana’s intransigence, the Trump administration has threatened to impose crippling new secondary sanctions on foreign companies doing business in key sectors of the Cuban economy. This is not just a story about Washington’s choices, however. For decades, the island’s government has prioritized internal control and external patrons over political and economic transformation. The onus to avert catastrophe is now on Havana. The longer Cuban leaders treat the path forward as a matter of revolutionary dignity rather than national survival, the more certain it becomes that whatever follows will be worse.

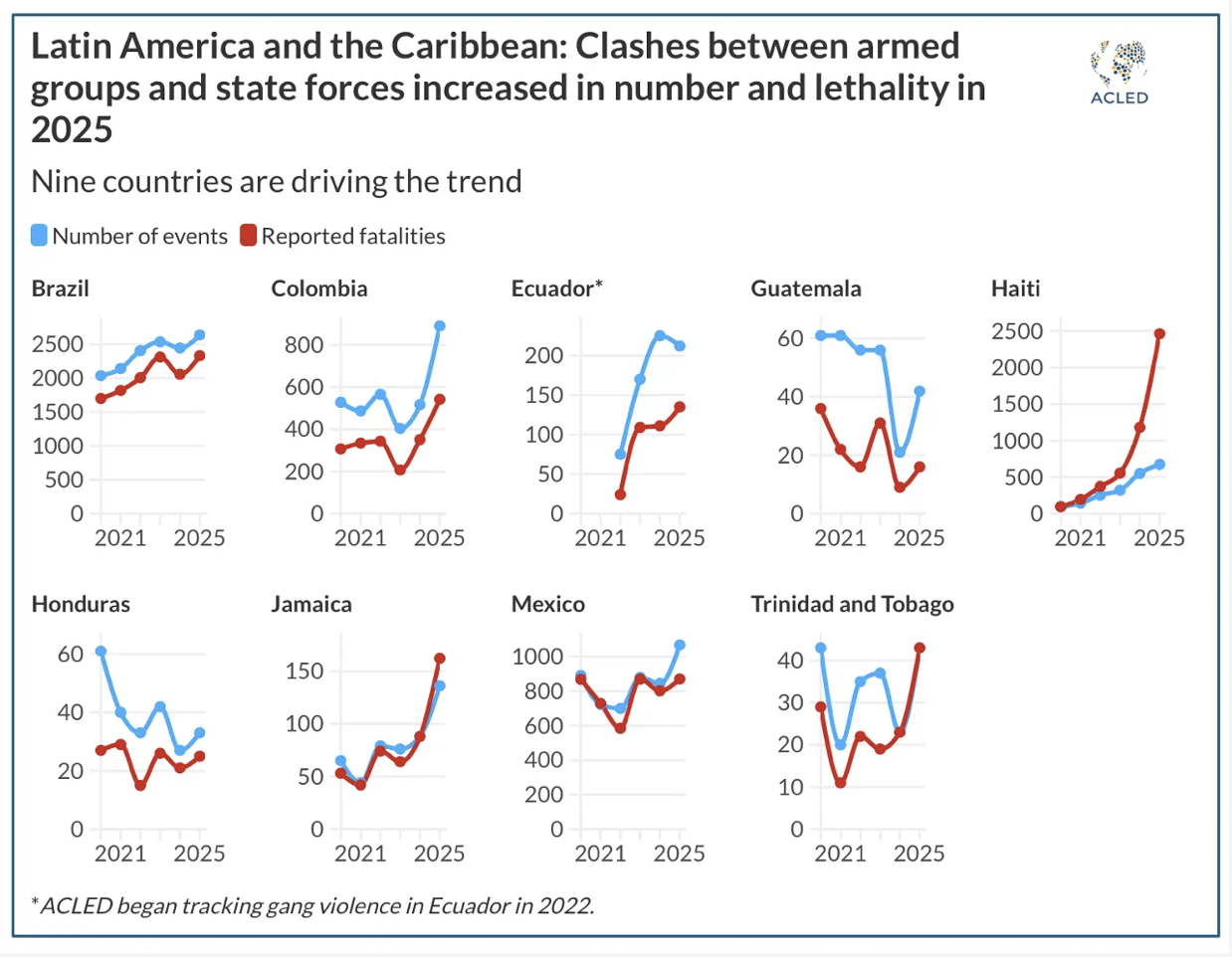

The US’ Donroe Doctrine is reshaping conflicts in Latin America and the Caribbean ACLED (Armed Conflict Location & Event Data)

The US has escalated its use of direct military force with governments it perceives as failing to meet its policy objectives, but direct military interventions are less likely during the remainder of President Donald Trump’s administration, which favors bilateral agreements or forced negotiations secured through pressure and threats. US pressure on organized crime is accelerating the spread of militarized security approaches in the region, which has had a number of knock-on effects:

The number and lethality of clashes between security forces and armed groups have surged, and the approach has fostered an environment of impunity for security forces.

Violence has decreased in areas where criminal groups have more limited resources, but gangs have responded by relocating, scaling back visible activities, and turning to selective forms of violence.

Armed groups have fragmented, increasing competition in countries where organized crime groups’ revenue sources are more diversified.

Recommended Weekend Reads

A Deeper Dive Into Cuba, Europe’s Critical Mineral Dependency Trap, The Geography of Start-Ups During COVID, and the Case for Data Centers in Space

May 22 - 25, 2026

Happy Memorial Day Weekend! Hopefully, you will get a little time to rest and read. Below are a number of reports and articles we read this past week and found particularly interesting. Hopefully, you will find them of interest and useful as well. Have a great weekend.

Cuba

The Secretive Conglomerate that Controls Cuba’s Economy The New York Times

The most powerful entity in Cuba is not the Communist Party. It is a secretive military-run conglomerate known as GAESA which is estimated to control between 40 percent to 70 percent of the Cuban economy. It is a commercial empire established by Raul Castro – brother of the late dictatorial leader Fidel Castro – to bolster the military. Today, it controls the finest hotels, restaurants, most of the gas stations on the island, the internet, and supermarkets. The New York offers a comprehensive, inter-active report on who exactly runs GAESA and just how sprawling an empire it is.

In Cuba, Socialism Has Morphed Into A Racket: What I saw on the island that once considered itself the future Persuasion (Substack by James Bloodworth)

The author traveled to Cuba recently, touring the capital, Havana, and was appalled by what he found. In the past, apologists for the Cuban government, wanting to show that the people have enough to live on, would point to the monthly ration book—the libreta—through which Cubans received a basic food basket. But since Raúl Castro succeeded Fidel in 2008, the ration book has been steadily pared back. Today it supplies, on average, enough to subsist on for perhaps 10 days at most, and only with careful rationing. Everyday items such as toothpaste and shampoo have disappeared from it altogether. In their place is the unforgiving market: a tube of toothpaste can now cost as much as 600 pesos, around 15 percent of a typical monthly salary. That is the equivalent of spending something like $800 on a single tube.

The Dilemma Over Cuba’s Future El País

Between grandstanding, contradictory statements, and secret meetings, something is happening in Cuba. A path has opened that is still full of unknowns, but one that now seems hard to reverse. In recent days, events have accelerated with the unusual visit by the CIA chief to Havana, the U.S. indictment of Raúl Castro — the Cuban Revolution’s last great symbol — and the deployment of an aircraft carrier in Caribbean waters near the island. As to what is likely to happen next, the precedent in Caracas looms over the island, but analysts and historians see a horizon of ‘capitalism without democracy’ as more likely than regime change.

Cuba’s Soviet-Era Military Could Still Complicate U.S. Operations in a Caribbean Crisis Global Defense News

Recent U.S.-Cuba tensions have sharpened a practical military question: what Cuba’s armed forces could actually bring to bear in a crisis with the United States, and which assets would matter first. Cuba’s Revolutionary Armed Forces remain built for territorial defense, relying on Soviet-era ground equipment, layered but aging air defenses, limited combat aviation, coastal patrol forces, and mobilization manpower. A 2025 profile estimates about 50,000 active armed forces personnel, with mandatory service for men aged 17 to 28, a 24-month obligation in the armed forces or Interior Ministry, and reserve liability for men until age 45. Older open-source military tables give lower regular army figures, around 38,000 active and 39,000 reserve personnel, illustrating the uncertainty that surrounds Cuban force accounting. The important point is functional rather than numerical: the FAR is designed to combine regular units, territorial militias, internal-security forces, dispersed storage sites, and local defense zones. In practical terms, that means Cuba’s military value is concentrated in delaying, absorbing, dispersing, and imposing local costs, not in matching U.S. joint forces in mobility, air power, naval reach, or precision strike.

Europe’s Competitiveness Challenge

Out of the Dependency Trap: Why Germany’s and Europe’s Critical Raw Materials Policy Falls Short and How to Fix It Global Public Policy Institute

We find that Germany and Europe’s policy approaches are still too strongly based on the false assumption that improving framework conditions for private-sector projects in Europe and elsewhere in the world will suffice to drive supply diversification. This assumption is misaligned with the reality of China’s state-backed, vertically integrated dominance that allows Beijing to shape prices and supply conditions. As a result, policies focused primarily on stimulating supply through permitting reform, financial derisking and project support in partner countries are insufficient. Other players such as Japan and the United States (US) have responded with greater resolve, deploying tools such as coordinated offtake agreements and price-support mechanisms to actively shape market dynamics. Europe’s failure to take similar steps reflects persistent misconceptions about global CRM markets, alongside fragmented and insufficient capacity in public institutions and a weak CRM ecosystem. Past efforts along four policy levers – (1) stockpiling, (2) expansion of primary supply, (3) expansion of recycling, and (4) demand reduction – exhibit a range of shortcomings, among which one stands out: the absence of stable, long-term demand at price levels that make investment in diversified supply chains in Europe and partner countries commercially viable. Without addressing this demand-side gap, even well-designed supply-side measures will fail to unlock the investment required.

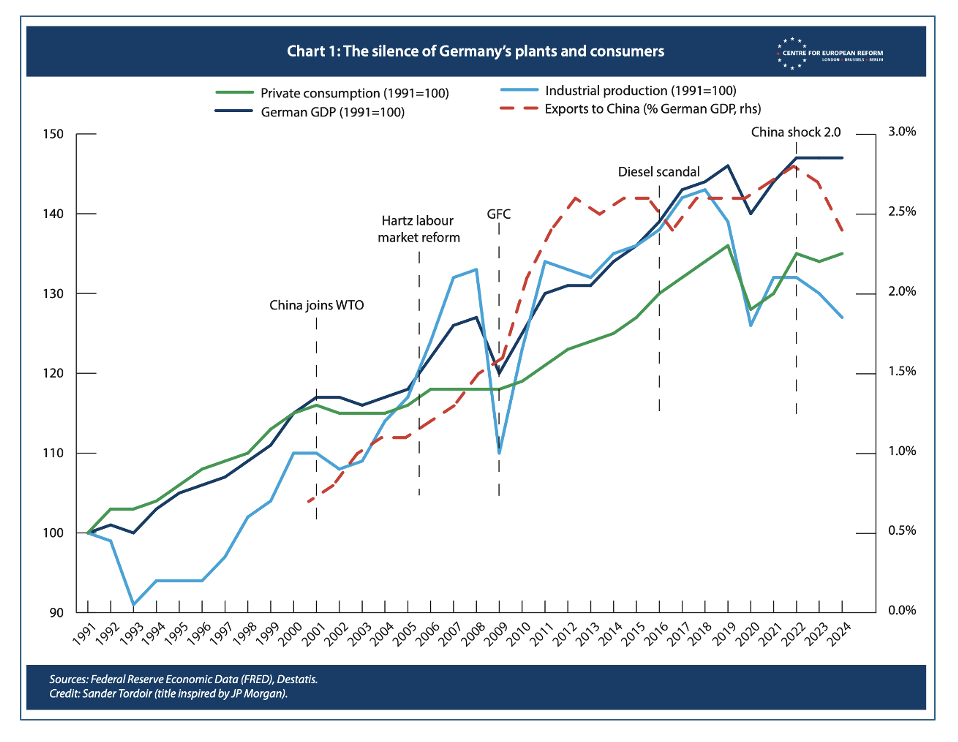

China Shock 2.0: The Cost of Germany’s Complacency Brad Setser/Sander Tordoir, Centre for European Reform

There is a growing consensus a new China shock is reverberating across global goods markets. Nowhere is that shock more consequential than in Germany. Its manufacturers in core industries – cars, machinery, chemicals and aircraft – are being simultaneously squeezed out of China and other foreign markets, and at home. The shock is worsening. Analysts had estimated China would only export 10 million cars a year by the end of the decade. But China’s 2025 fourth quarter exports, annualized, already hit that mark. The car sector is not unique. In 2025, China’s overall export volumes grew at more than twice the pace of global trade. And they gained strength in early 2026, with first quarter export volume growth at 15 per cent. The risk for Berlin, which already struggled to adjust when China’s surplus jumped from 2 to 5 per cent of GDP from 2022 to 2025, is acute. Germany faces a structural demand shock from a state-distorted rival that cannot be addressed like past competitiveness challenges: Berlin and Brussels must either bolster their trade defenses and industrial policy or prepare to offset the social and economic costs of deindustrialization at China’s hand.

How can Europe shape the Iran war’s aftermath? Nathalie Tocci/Brookings Institution

The U.S.-Israel war against Iran, encompassing the Persian Gulf and Lebanon, has revealed Europe at its worst. Looking ahead, it could also see Europe at its best. The war in Iran is laying bare a long-standing reality: Europe’s attachment to multilateralism and international law has been rooted as much in interests as in idealism. If Europeans genuinely internalize this lesson, they must be willing to act on it in concert with Gulf and Asian partners in shaping the postwar order. This neither means decoupling nor closing the door to the United States. Rather, as multilateral initiatives are planned and hopefully implemented in the region, the door should remain open for the day Washington chooses to step in.

Dawn of the Electric World Order Kate Maackenzie/Tim Sahav – Phenomenal World (Substack)

Oil and gas—the foundation of global systems of energy and production—are no longer reliably available where and when they are needed at bearable prices. Two wars in four years have triggered a permanent risk regime shift. No matter how uneven and uncertain the immediate reaction from markets and governments, the lesson of the present energy shock is unavoidable: the geopolitical conditions that once stabilized the carbon-based logistics of the modern world can no longer be guaranteed, and electrification offers a structural exit from instability. After two months of war and supply chain disruption, the situation is becoming desperate in much of Asia and Africa and roiling across Europe and the Americas. Many oil and gas importing countries are now being forced to triage: how much LNG goes to power generation versus fertilizer plants? Bidding wars will leave those without deep pockets paying in increased hunger, lost wages, and shrinking economies. It’s not just oil being affected by the war. From cooking gas to fertilizers to sulphur to helium, the war has yet again exposed the material underpinnings of the global economy and its web of interdependence. Where does this leave Europe?

Geoeconomics, AI, and Start-Ups

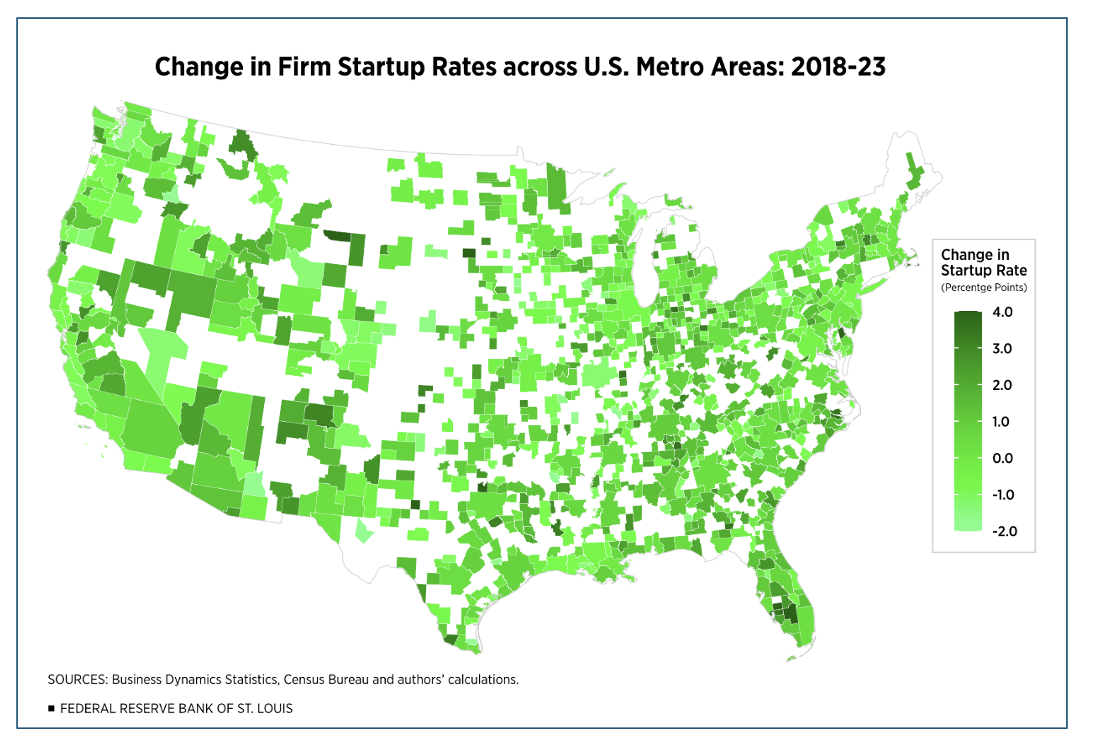

The Geography of the Startup Surge During the Pandemic Federal Reserve Bank of St. Louis

After sharply declining since the late 1970s, the firm startup rate began to steadily rise in the 2010s, with a shift toward larger cities. Startup activity then accelerated during the COVID-19 pandemic. Where did this pandemic-era growth occur? Startup growth during the pandemic was spread widely across U.S. regions instead of being concentrated in coastal tech hubs. While bigger cities continued to have higher startup rates, business formation rose across all city sizes.

The Jevons Paradox and Insatiable Humans: Why AI Won’t Empty the Finance SuiteEldar Maksymov/Arizona State University (ASU) - School of Accountancy

Abstract: The conversation around AI and white-collar work has fixated on the wrong question. Anthropic’s March 2026 finding that AI can theoretically perform 94.3 percent of business and finance tasks has executives debating which jobs will survive. They should be asking which jobs are about to come into existence. The Jevons Paradox—William Stanley Jevons’s 1865 observation that efficiency gains expand rather than contract resource use—provides the framework. Its cleanest modern test: U.S. accountants quadrupled between 1980 and 2022, growing at nearly seven times the rate of population growth, after spreadsheets automated their core work. AI is to today’s accountant what VisiCalc was to 1980’s—except more powerful. The near-term displacement is real and painful. But firms that treat AI only as a headcount-reduction tool will miss the expansion. This article maps that expansion and offers concrete prescriptions for students, executives, and educators.

The Commercial Space Race

Old Space, New Space: A Commercial Revolution in Innovation? Ruben Gaetani and Alexander T. Whalley National Bureau of Economic Research

The biggest post-1970s surge in space innovation came in the 1990s, when policy created commercial markets for satellites and communications. Incumbent firms, not “New Space” entrants, drove most of this boom and still account for most space patents. This paper uses patent data to examine the timing and composition of space innovation, finding patterns that challenge the popular narrative attributing commercial space transformation to entrepreneurial entrants after 2005. Our findings reveal that the commercial space transformation is more closely connected to its government-led origins than narratives emphasizing entrepreneurial disruption suggest.

“I’ll buy 10 of those”—NASA science chief yearns for mass-produced satellites ARS Technica

There are more opportunities to access space than ever, thanks to a bevy of commercial rockets, some with reusable boosters, led by SpaceX’s workhorse Falcon 9. So why is NASA launching fewer telescopes and planetary science missions than it did a quarter-century ago? The answer is complex. It is not necessarily the money. The space agency’s science budget this year is $7.25 billion, roughly the same as it was in 2000, adjusted for inflation. This is despite attempts by the Trump administration to drastically reduce NASA science funding.

The case for data centers in space: An Interview with Starcloud CEO Philip Johnston McKinsey

As demand for AI compute rapidly accelerates, space-based data centers have the potential to move from concept to early deployment. In practical terms, this involves packaging servers and supporting systems into space-qualified modules, powered primarily by solar energy, managing tempo, and connecting back to Earth through high-bandwidth communications links. In theory, space-based systems could offer both structural advantages, such as unconstrained energy scaling and higher solar efficiency, but also the potential for cost competitiveness with terrestrial systems. Questions remain, however, about whether space-based compute can deliver that in practice, offering predictable performance, repeatable deployment, credible reliability, and sustainable, competitive economics even after accounting for launch cadence, replacement cycles, and data-movement costs.

Recommended Weekend Reads

Putin and Russia Are Facing Rough Waters, How Mexico Benefits From the US – China Trade War, Will Raising Taxes Solve the US Debt Problem? And How America is Experiencing a Productivity Miracle

May 15 - 17, 2026

Below are a number of reports and articles we read this past week and found particularly interesting. Hopefully, you will find them of interest and useful as well. Have a great weekend.

Russia

Putin Is Losing His Grip on Russia The World Unpacked Podcast

Russia’s surprising recent Internet shutdown did more than disrupt daily life: it also crippled the regime’s own communications and propaganda. It’s one of a series of strange events—from a diminished Victory Day parade to crackdowns on businesspeople and celebrities—that suggest growing disorder and confusion within the Russian state. Alexandra Prokopenko, a former Moscow insider who quit over the Ukraine War, says that Vladimir Putin has lost focus on running the country. She joins Jon Bateman on The World Unpacked to explain the erosion of Russia’s social contract and share stories from her new book, From Sovereigns to Servants: How the War Against Ukraine Reshaped Russia’s Elite.

In Russia, the Public Mood Is Souring Carnegie Russia Eurasia Center

Something in the air has changed in Russia. Now even loyalists complain about the mounting restrictions and repression, and once-upbeat businesspeople are now despondent. What we are witnessing is three related processes. First, attitudes toward President Vladimir Putin are changing. Second, economic optimism and the associated everyday patriotism, which celebrates survival rather than development (people are simply grateful to be alive) are fading. And finally, Russian people are realizing the impossibility of winning a war that has minimized their country’s advantages.

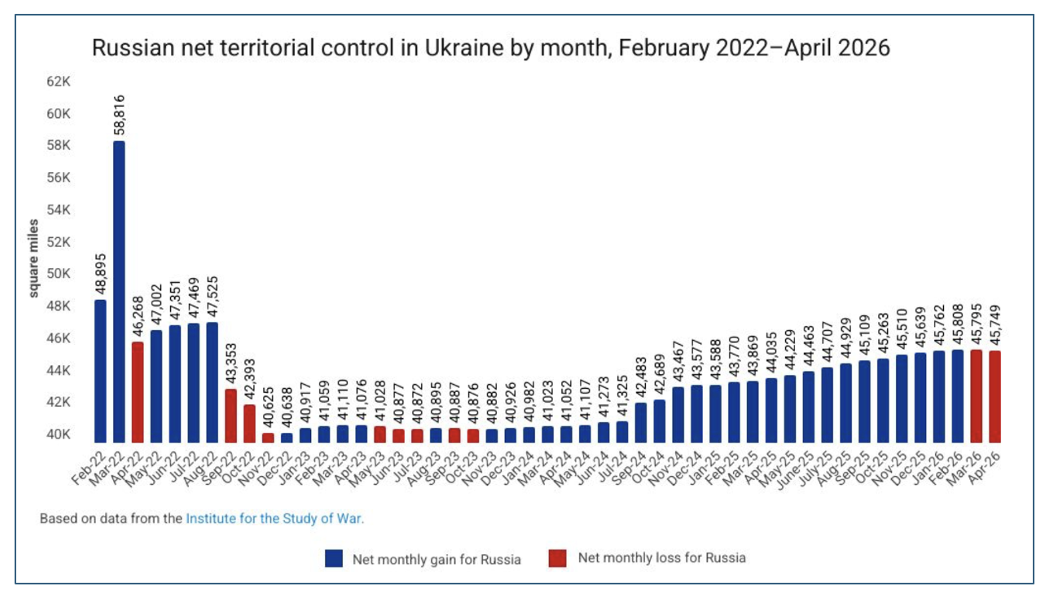

The Russia-Ukraine War Report Card, May 13, 2026 Russia Matters

May 12, 2026, update: Russia Matter’s analysis of ISW’s data for the past four weeks (April 14–May 12, 2026) indicates that Russian forces endured a net loss of 45 square miles (about twice the size of Manhattan Island) of Ukraine’s territory during that period. This contrasts with the previous four-week period (March 17–April 14, 2026), in which Russian forces lost a single square mile of Ukraine’s territory. In the past week (May 5–12, 2026) Russia recorded a net loss of 12 square miles (about half of Manhattan Island). Notably, Russia launched more than 8,000 drones last month, the highest monthly total on record since the start of its full-scale invasion of Ukraine on Feb. 24, 2022, according to data published by CSIS since September 2022 and analyzed by RM. Meanwhile, FT reported, citing two people in contact with Vladimir Putin and a Ukrainian intelligence assessment, that Russia’s top commanders have convinced Putin their forces could seize the whole of the Donbas by this fall. Since the beginning of the war, RM and other analysts estimate Russia has military losses of more than 1,000,000 men, 14,000 tanks and armored vehicles, 361 aircraft, and 29 naval vessels.

War, Inflation, and Putin’s Paranoia: Has Russian Public Opinion Begun to Shift? Russian Roulette (Center for Strategic and International Studies Podcast)

Dr. Sam Greene, professor of Russian Politics at King’s College London, discusses the state of Russian public opinion today and whether domestic conditions have begun to change given the state of the economy, war, and reportsof increasing paranoia in the Kremlin.

Geoeconomics

America Is Experiencing A Productivity Miracle Economist Staff The Economist

The 2019–2024 uptick in US productivity wasn’t driven by the information sector, whose growth and scale is on par with its 2000–2019 mean, but rather by professional services and management, which together make up ~10% of the economy.

The Microstructure of AI Diffusion: Evidence from Firms, Business Functions, and Worker Tasks National Bureau of Economic Research

Abstract: Using novel, nationally representative data from the 2026 AI supplement to the U.S. Census Bureau’s Business Trends and Outlook Survey (BTOS), we characterize AI diffusion across three layers: firm-wide adoption, business-function deployment, and worker-task use. During Nov 2025–Jan 2026, 18% of firms used AI in at least one function (32%, employment-weighted), with adoption expected to reach 22% within six months. Use is concentrated in large firms and knowledge-intensive sectors, reaching 50%–60% (60%–70%, employment-weighted) among very large firms in Information, Professional Services, and Finance. Among adopters, scope remains limited: 57% use AI in three or fewer functions, most often Sales and Marketing (52%), Strategy (45%), and IT (41%). Worker-level use appears in 23% (41%, employment-weighted) of firms, primarily for writing, document analysis, and information search; 65% restrict use to three or fewer tasks. Evidence suggests both top-down and bottom-up diffusion: worker use can occur without firm adoption, and vice versa. Most firms (66%) use AI for task augmentation, while employment reductions are rare (2%). Regression results show a positive relationship between firm performance and AI integration breadth. However, functional deployment and operational investment are associated with employment declines, while worker-task use is not once these factors are controlled for.

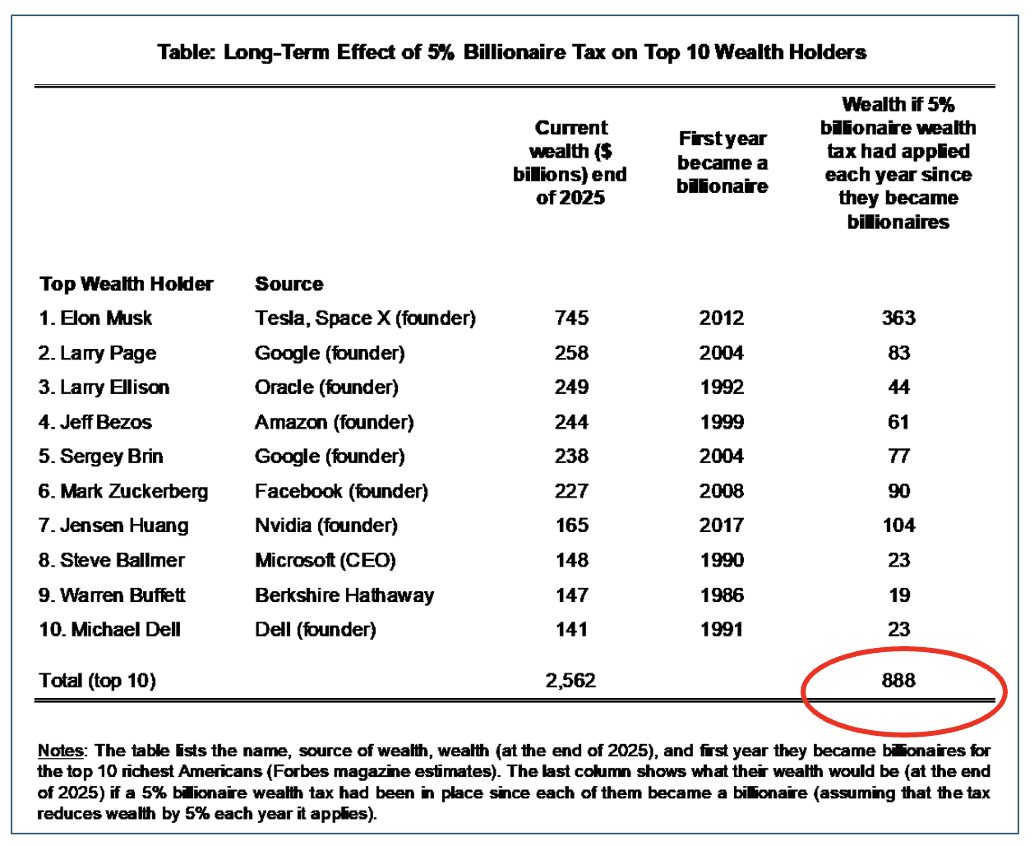

Can Tax Reform Solve the Debt Problem—or Just Slow It? Tax Foundation

The US federal government faces several fiscal challenges in the coming decades, as the Congressional Budget Office projects that, under current law, publicly held debt as a share of GDP will rise to a new record high within the next four years and continue rising to 175 percent of GDP by 2056. While revenues are projected to grow as a share of GDP, spending will grow faster so that deficits rise to 9.1 percent of GDP by 2056. This study simulates several large tax increases and consistently finds that even tax increases large enough to close the primary deficit in the near term will lose ground over time and fail to put the debt on a sustainable course. The most popular proposals, from hiking taxes on the rich to raising tariffs, tend to target a narrow set of taxpayers and produce the least sustainable revenues. These options are likely to introduce large economic distortions and slow economic growth without substantially improving the debt trajectory. The results suggest deficit reduction efforts should focus first on reducing the growth of major entitlements, and second on relatively efficient, broad-based tax increases.

Latin America

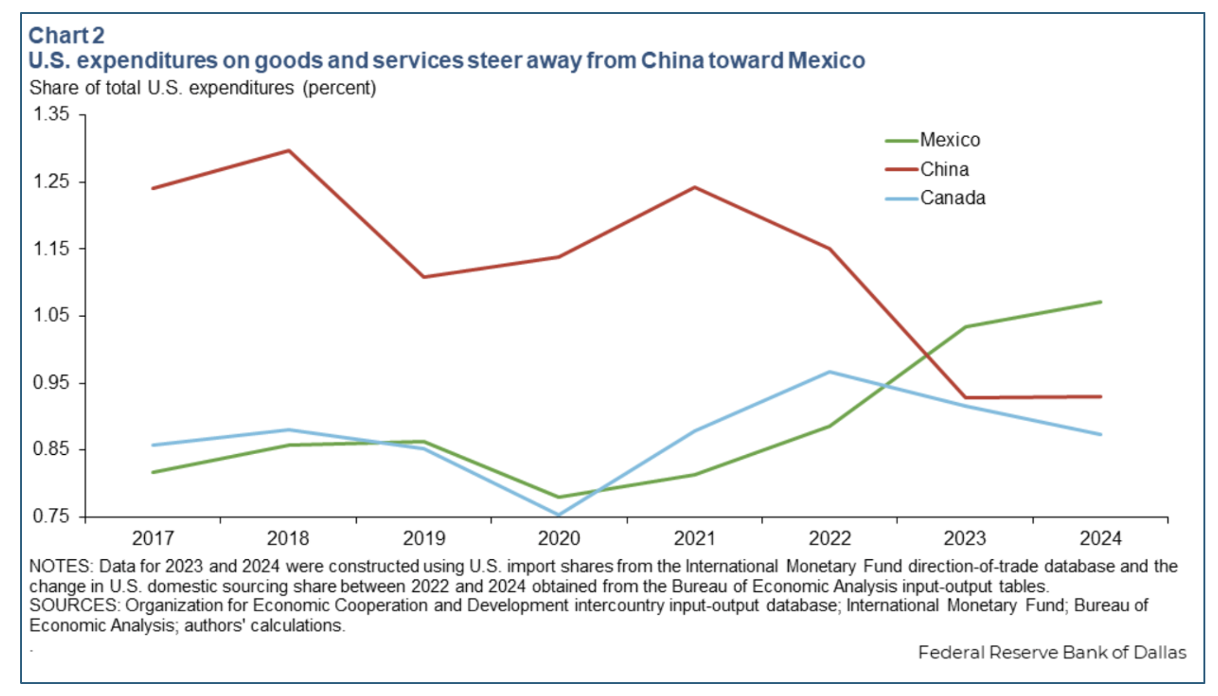

Mexico Gains From U.S.-China Trade War; Inefficiencies Limit Benefit Ricardo Reyes-Heroles, Luis Torres and Diego Morales-Burnett Federal Reserve Bank of Dallas

Abstract: We examine the effects of the tariffs implemented during the U.S.-China trade war on Mexico’s GDP, using a multi-country, multi-sector general equilibrium trade model. Higher U.S. tariffs on Chinese goods reduce the competitiveness of Chinese exports in the U.S. market, thereby shifting U.S. demand toward alternative suppliers, including Mexico. Model simulation indicates the U.S. - China tariff shock generated a positive effect on Mexico’s GDP, shifting U.S. demand from goods produced in China toward those produced in Mexico. There was a clear increase in U.S. demand for goods produced in Mexico during 2017–24, suggesting that output in Mexico expanded to meet this increased demand in response to the China trade tension. In the medium run—a period when aggregate capital does not change through investment—Mexico experiences a modest increase in GDP of 0.35 percent, driven primarily by higher exports to the United States and expansion of sectors integrated into North American value chains. Once Mexico’s capital stock adjusts, GDP expands by an additional 0.73 percentage points (total of 1.08 percent), reflecting increased investment in expanding industries (Chart 3). Although trade reallocation has contributed to economic growth in Mexico, structural constraints led to underperformance.

The Strategic Link Between USMCA and Critical Minerals Arturo Sarukhan/Americas Quarterly

Critical minerals have emerged as one of the issues most likely to define what the “new USMCA” stands for: not merely a trade agreement, but the enforcement spine of a broader hemispheric economic-security strategy that integrates market access, technology governance, and supply chain integrity. If the review produces a meaningful minerals annex—or a trilateral minerals side agreement—it will represent a genuine architectural advance. If it fails to do so, the continent risks locking in bilateral templates.

Unpacking Peru’s First-Round Elections 35 West Podcast

On April 12, Peruvians took to the polls to vote in the first round of elections that would decide the country’s next president. Some hoped the elections would help usher in an end to the country’s long running political crisis where no president has served out a full term since 2016. However, delays and complications in counting the votes, and fraud allegations leveled by some candidates turned the April election into its own miniature crisis. In this episode, Henry Ziemer sits down with Mitra Taj, a freelance reporter based in Lima to unpack the results of the first round of voting. Together they explore the key figures and power brokers heading into the runoff, as well as how the two candidates, Keiko Fujimori and Roberto Sánchez, will likely approach key issues of economic development, security policy, and relations with Congress. They also explore the significance of the elections for ongoing U.S.-China competition in South America.

The prediction markets are betting on Colombia’s upcoming election Latin America Reports

Prediction market giants Kalshi and Polymarket are showing a recent surge in bets on right-wing populist Abelardo de la Espriella to be the eventual winner of Colombia’s presidential election at the end of May. The markets are out of line with conventional polls in Colombia, which have leftist candidate Ivan Cepeda comfortably leading the race with de la Espriella in second, followed by center-right candidate Paloma Valencia. In the last week, however, bets on de la Espriella to win the election have increased relative to bets on his rivals. On May 1, de la Espriella was given a 28.8% chance of victory whilst Cepeda was given 38% on betting market Kalshi. As of May 8, de la Espriella has overtaken Cepeda by 1 percentage point, reaching 42%. Polymarket shows a similar trend. De la Espriella’s odds have risen from 28% to 39% over the last seven days, though he still trails Cepeda, who remains on 41%.

How America Can Coerce the Cartels Benjamin Lessing/Foreign Affairs

There is an alternative to the ongoing violent response to Latin American drug cartels: It is what the author calls “conditional repression.” Countries facing powerful and destructive criminal groups, such as drug cartels and prison gangs, should draw bright redlines and concentrate their fire on the groups that cross them. Escalatory measures, whether military or judicial, could be used to punish only the worst cartel behavior. In this way, the repressive force that is currently failing to stop the drug trade could be used coercively to reduce its most pernicious harms. And nobody understands coercion better than Trump. From tariffs to military operations in Iran and Venezuela, he has seized personal control over levers of power and used it to punish those who do not bend to his will. Trump could do the same to cartels: cow them into ending fentanyl flows and minimizing violence, criminal governance, civilian extortion, and environmental degradation. However contentious his tactics, this president may be uniquely (and surprisingly) qualified to change the way the United States—and the world—fights the drug war.

Recommended Weekend Reads

Previewing the Trump – Xi Summit, Overcoming Latin America’s Stubborn Productivity Gap, Who Will Make Money on AI?, and How Americans Rarely Talk to Their Neighbors

May 8 - 10, 2026

The US and China in Advance of the Xi–Trump Summit

In What Ways Has U.S. Trade with China Changed? Hunter Clark and Gregory Simitian - Federal Reserve Bank of New York

In 2025, the US deficit with China in machinery and electrical goods fell ~$70 billion, while the US deficit with ASEAN in similar goods rose ~$80B, and China’s surplus with ASEAN increased ~$70 billion — reshuffling, not shrinking, trade imbalances.

What will happen when Trump meets Xi? Brookings Institution Expert Roundtable

President Donald Trump will travel to Beijing for meetings with President Xi Jinping on May 14-15, 2026. Nine Brookings experts weigh in below on how Trump and Xi’s interaction will impact their areas of expertise and how the summit’s success will be measured. But as Ryan Haas, Brookings Director of the John L. Thorton China Center, suggests, observers should have low expectations for the upcoming summit. While the relationship has stabilized since the two leaders met last November, Haas points, it remains fragile—defined more by an absence of friction than any affirmative agenda or deep dialogue on the substantial differences that bedevil the relationship. Many Chinese analysts expect a U.S. snap back to a more competitive China policy, either after the midterms or after Trump steps down in 2029. Beijing seems focused on using this interregnum to enhance its position vis-à-vis the United States. Likewise, many in the Trump administration and on Capitol Hill favor a return to sustained strategic competition.

Americans’ views of China have grown somewhat more positive in recent years Pew Research Center

For the better part of a decade, most Americans have had negative views of China. This is still the case, but the share with a favorable view has ticked up, according to a Pew Research Center survey conducted in March. Today, 27% of Americans have a positive opinion of China. That has risen 6 percentage points since last year and nearly doubled since 2023. And it’s part of a modest softening of Americans’ opinion of China on multiple fronts:

Confidence in Chinese President Xi Jinping to do the right thing regarding world affairs has gone up 4 points since last year and roughly doubled since 2023.

When asked whether China is a partner, enemy or competitor of the United States, fewer Americans call China an enemy now than in 2025. But most Americans still see it as a competitor.

Slightly fewer say now than last year that China is benefiting from trade at the expense of the U.S.

China’s Demographic Future Is Now The Rhodium Group

We estimate China will lose nearly 60 million people in the next decade, roughly equivalent to the population of France. The impact on household consumption is obvious, but the larger problem for Beijing may be the hit to social security funds. The headlines are bad, the regional breakdown is worse. The country’s most developed provinces are seeing falling populations, which will impact overall consumption and the future productivity of the labor force. The impact on household consumption is obvious, but the larger problem for Beijing may be the hit to social security funds. The fiscal subsidy to social security funds rose to a record 2.9 trillion yuan last year, or 10.1% of general budget spending, and appears set to rise in the future.

Latin America

A Bad USMCA Rewrite Will Cost Mexico More Than No Deal Juan Pablo Spinetto/Bloomberg

The USMCA free-trade pact is due for review on July 1, with negotiations likely to run past the deadline and potentially leading to annual reviews. Mexico has high stakes in the review, with an updated USMCA potentially lifting uncertainty and unlocking investments, but the country should resist sacrificing a good deal for a quick one. Mexico should secure explicit guarantees that US tariffs on certain goods will be lifted or reduced before making any announcements, and may be better off waiting for a shift in Washington’s stance if such guarantees are not provided.

Sinaloa Governor Indicted: USMCA, Cartels, and the Future of U.S.-Mexico Trade Center for Strategic and International Studies

On April 29, Sinaloa Governor Rubén Rocha Moya and nine other current and former Mexican officials were indicted by the U.S. Department of Justice on charges of conspiring to assist the Sinaloa Cartel in trafficking drugs into the United States in exchange for bribes and political support. The move was not a surprise, but a culmination. For 18 months, the White House had been turning the screws on the Sheinbaum administration, demanding deeper security cooperation and tangible outcomes, while holding a series of escalating threats in reserve, among them the specter of unilateral U.S. military action on Mexican soil. Mexico responded at nearly every turn—yet the goalposts moved. The indictment of sitting officials from Morena, Mexican President Claudia Sheinbaum’s party, represents one of the most consequential of those threats, one that the White House had kept in reserve but never fired. Its timing is not incidental. It comes at a moment of acute bilateral tension, and just weeks before the formal review of the United States–Mexico–Canada Agreement (USMCA), currently scheduled to launch, without Canada, on May 26.

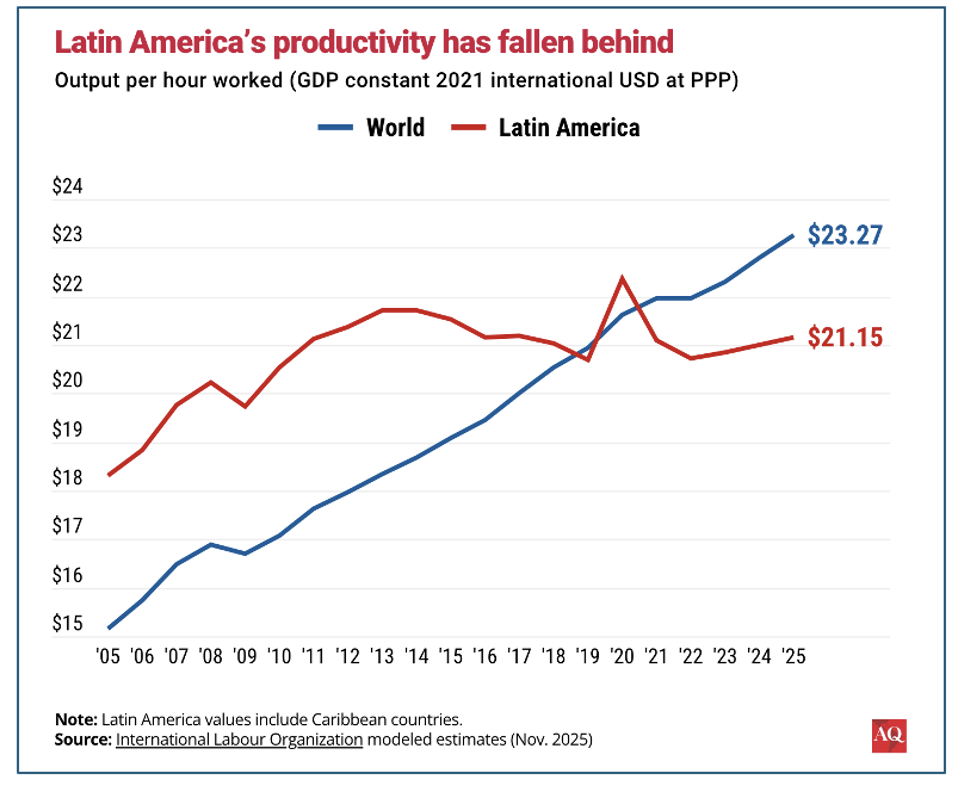

Overcoming Latin America’s Stubborn Productivity Gap Americas Quarterly

Call it Latin America’s perennial challenge: Low productivity. Measured as output per worker or per hour, productivity in most of the region remains a fraction of that in advanced economies and has hardly improved over the past 75 years. The result is a development constraint that scholars and observers use to explain why Latin America and the Caribbean are currently immersed in a “low growth trap” that limits wages and political stability alike. A growing body of research has identified the persistent culprits, but also the solutions that we urgently need. Low productivity limits the region’s ability to capitalize on new global opportunities—including those emerging from today’s rapidly shifting trade environment.

Geoeconomics, Statistics, and The Global Growth of AI

The Value of Reliable Statistics Nicholas Bloom/Erica Groshen/Duncan Hobbs/Michael Strain – NBER Working Paper Series

Abstract: On August 1, 2025, President Trump fired the head of the U.S. Bureau of Labor Statistics (BLS) and claimed that the agency’s data were “rigged.” In the aftermath, measures of economic policy uncertainty rose sharply, consistent with the idea that reduced trust in official data increases uncertainty for investors, businesses, and households. We use an event-study design to estimate the effect of the firing on policy uncertainty and then map that increase in uncertainty into implied macroeconomic outcomes. This yields a back-of-the-envelope estimate of the marginal value of public trust in official statistics. Our baseline estimate implies that preserving trust in the integrity and quality of official statistics generates economic benefits of about $25 for every $1 spent on the agency’s budget.

Who Will Make Money on AI? A Discussion Paper on Aligning Commercial Incentives with National Security Interests Geoffrey Gertz and Emily Kilcrease/Center for a New American Security

The private sector is playing a leading role in advancing the frontier of artificial intelligence (AI). As a result, commercial incentives are likely to have a significant impact on how AI capabilities develop and diffuse across markets. Firms’ commercial incentives will influence U.S. national security interests associated with the emergence of powerful AI systems. These interests include enabling beneficial uses of AI while limiting security risks associated with AI misuse, ensuring reliable and controllable AI system behavior in deployment, and maintaining strategic geopolitical advantage in the development and global diffusion of AI. Yet to date, stakeholders focused on AI national security interests have paid only limited attention to AI companies’ commercialization strategies and market dynamics across the AI stack. This paper seeks to bridge this gap, identifying potential scenarios for the future shape of AI markets and exploring the implications of these scenarios for U.S. national security. Rather than attempting to resolve core debates on the commercialization of AI, the paper seeks to prompt consideration in both the private and public sectors, and among economics and national security expert communities, of how commercial incentives can better align with U.S. national security interests.

The Sovereign AI Index – Tracking the Global Push for AI Self-Reliance Center for a New American Security

CNAS is running an interactive, regularly updated site tracking the explosive growth of AI globally. As they point out, The United States and China control 90 percent of the computing power needed to develop and deploy frontier AI. They own all 50 of the top-ranked AI foundation models. Concerned about this concentration of AI power, governments worldwide have responded with initiatives to strengthen their AI capabilities under the banner of “sovereign AI.” Although a consensus definition of sovereign AI remains elusive, this index defines a sovereign AI project as a government-backed AI initiative tied explicitly to national strategic interests and backed by material public investment in domestic compute, models, or data ecosystems. The drivers of sovereign AI vary widely. For some countries, the imperative is security: protecting sensitive data and ensuring access to advanced capabilities for defense and intelligence. For others, it is the economy: leveraging AI to spur AI-related local investment, jobs, productivity, and long-term value. Culture is another driver, with nations seeking AI systems that better reflect local languages and norms. Autonomy also motivates countries that see danger in growing AI dependence on the United States or China. These drivers often overlap. The result is a surge in sovereign AI activity across the globe.

An American industrial revolution is brewing. I saw it in Pittsburgh. David Ignatius/Washington Post

Columnist and former Business Editor Ignatius went to Pittsburgh to witness first-hand an extraordinary change taking place. Watching a nimble robot check for flaws along the side of a massive steel tube crafted to simulate the reactor of a nuclear submarine, you see a snapshot of the revolution in manufacturing and maintenance that could transform the gritty, routine tasks of the defense industry — and perhaps American manufacturing, as well.

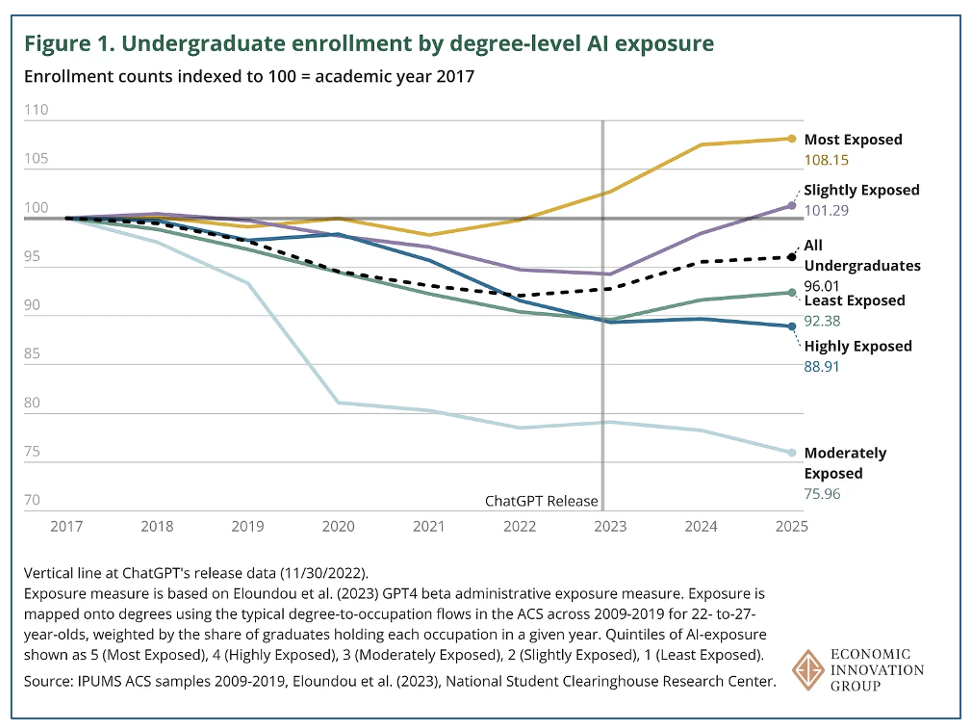

How Students and Recent Grads are Responding to the Rise of AI Sarah Eckhardt and Nathan Goldschlag/Agglomerations

Far from shying away from AI, American undergraduates “are flocking towards the most-AI-exposed degrees,” with enrollment in these majors up 8% last year compared to 2017. Are students shying away from fields that have more exposure to AI, perhaps worried that AI will shrink the number of jobs available to them? Or are students shifting towards those fields, preparing for a future in which they will have to be comfortable using AI? To find out, we can check enrollment for groups of degrees based on the AI exposure of the jobs that students with those degrees are likely to take, as shown in Figure 1. As is clear, undergraduates are flocking towards the most-AI-exposed degrees, with enrollment in those degrees up 8% last year compared to 2017. This trend holds despite a notable decline in Computer Science degrees, one of the most-AI-exposed degrees, but whose decline is more than offset by increases in other exposed degrees like Engineering.

Societal Challenges in America

Strangers Next Door Daniel Cox, Jae Grace, and Avery Shields/American Enterprise Institute

In 2012, 51% of Americans aged 18–29 and 59% of all Americans spoke to their neighbors “at least a few times per week.” By 2025, only 25% of 18–29 year olds did relative to 40% of Americans overall. The effect was less pronounced for college grads.

Is America Financially Illiterate? The Numbers Are Alarming The Tax Foundation

In this podcast, Most Americans don’t understand how the tax code works, and it’s costing them. In this episode of The Deduction, host Kyle Hulehan sits down with Zoe Callaway, VP of Education at Tax Foundation, to talk about tax and financial literacy in America. They dig into the results of Tax Foundation’s national survey on tax literacy, the most stubborn misconceptions people have about taxes (including one that nearly made a teacher turn down her own promotion), and what’s happening in high school classrooms across the country. They also connect everyday tax confusion to bigger policy questions, from tariffs to tax refunds.

Recommended Weekend Reads

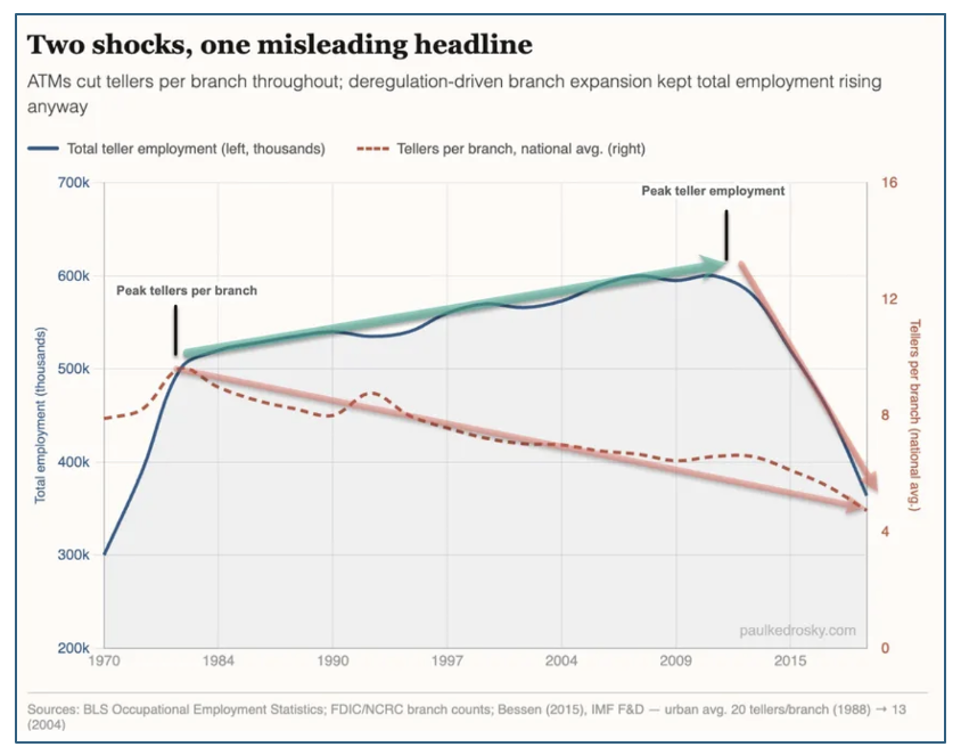

The Global Threat Assessment, The Iran War and What Comes Next, China – US Relations At an Inflection Point, and AI and the Fable of ATMs

March 20 - 22, 2026

Below are a number of reports and articles we read this past week and found particularly interesting. Hopefully, you will find them of interest and useful as well. Have a great weekend.

The Global Threat Assessment

The 2026 Annual Threat Assessment of the U.S. Intelligence Community Office of the Director of National Intelligence

The Office of the Director of National Intelligence (ONDI) – which oversees all 18 US intelligence agencies and organizations – this past week published it annual global threat assessment. The report details cybersecurity risks posed by nation-states to U.S. networks and critical infrastructure, as well as the increasingly sophisticated capabilities of cybercriminal ransomware actors. It outlines the current threat landscape, focusing on nation-state adversaries linked to the governments of China, Russia, Iran, and North Korea. The report also emphasizes the growing cyber espionage threat from Iran targeting U.S. networks and critical infrastructure.

The Iran War: Why Is It Happening and What’s Next?

You Can’t Print Molecules Jeff Currie and James Gutman Carlyle

When the dust settles and the strait reopens — partially, gradually, and perhaps on Tehran’s terms — the cost of rebuilding will likely be enormous. Governments must simultaneously finance defense, rebuild strategic reserves, restart domestic energy production, and harden infrastructure. All of this comes at a moment when inflation expectations are driving the cost of funding sharply higher — Germany’s 10-year bund auction technically failed this week, not for lack of liquidity, but because the bond market is already pricing the inflationary impact. Where does the capital come from? Capital will flow from the sectors that prospered during the era of open sea lanes and cheap energy, asset light, into the sectors that will build the replacement, asset heavy. The rotation back toward physical assets is not a trade — it is a regime change.

Tracking US Military Assets in the Iran War The Atlantic Council

The Forward Defense program of the Atlantic Council’s Scowcroft Center for Strategy and Security have just launched a new regularly updated tracker to analyze what the US military is committing to the war in Iran and what that means for a potential conflict with China. Operation Epic Fury is stressing military capabilities—aircraft carriers, bombers, missile defense systems—in ways that will have an impact in other theaters around the world. That includes US efforts to credibly deter Chinese aggression and prevail against China in a future conflict. Monitoring the military assets that are relevant to US strategy in the Indo-Pacific and currently deployed to Iran offers insight into how the war might affect the US military's readiness to meet the threat posed by Beijing—the most consequential challenge the United States faces. Actual numbers of US inventory and deployment data are classified. This tracker provides estimates for a subset of assets where open-source information is most reliable. It will be regularly updated and expanded with new data and expert context.

The Stunning Failure of Iranian Deterrence And Why It Augurs a More Dangerous World Nicole Grajewski & Ankit Panda/ Foreign Affairs

Although it was the United States and Israel that instigated attacks on Iran on February 28, leaders in Tehran deserve some of the blame for failing to effectively deter their adversaries. As the deceased commander of the Islamic Revolutionary Guard Corps Aerospace Force, Amir Ali Hajizadeh, once put it, maintaining deterrence is like riding a bicycle: “You have to keep pedaling all the time, or else the bicycle will fall.” Over the past three years, Iran started to lose its balance; now it has tipped over.

Why Escalation Favors Iran Robert Pape/Foreign Affairs

Iran’s military strategy cannot be dismissed as acts of scattered retaliation, the flailing lashing out of a dying regime. Rather, they represent a strategy of horizontal escalation, a bid to transform the stakes of a conflict by widening its scope and extending its duration. Such a strategy allows a weaker combatant to alter the calculus of a more powerful foe. And it has worked in the past, to the detriment of the United States. In Vietnam and Serbia, U.S. adversaries responded to overwhelming displays of American airpower with horizontal escalation, eventually leading to American defeat, in the former case, and, in the latter, frustrating U.S. war aims and spurring the worst episode of ethnic cleansing in Europe since World War II. Decapitation strikes, in particular, create powerful incentives for horizontal escalation: when a regime survives the loss of its leader, it must demonstrate resilience quickly by widening the conflict. Although the United States has hugely battered Iran, it must reckon with the implications of Iran’s response. Otherwise, it will find itself losing control of the war it started.

How Iran’s ‘forward defense’ became a strategic boomerang Chatham House

The war has exposed the limits of Iran’s long-standing strategy of ‘forward defense’. Worse still, that strategy has significantly contributed to Iran’s current predicament. So much so that, depending on the current conflict’s outcome, Tehran may need to fundamentally reconsider an approach to its security that it has refined, expanded and invested in for more than four decades. Since the 1980s, Iranian leaders have tried to push threats away from their borders by cultivating armed partners in fragile and divided Arab states. Through Hezbollah in Lebanon, militias in Iraq and Syria, Palestinian militant groups in Gaza and the Houthis in Yemen, Iran built a destabilizing network that allowed it to project influence while avoiding direct armed conflict with Israel and America.

China

Trump, Xi, and the Case for Strategic CalmRyan Hass/Foreign Affairs