Fulcrum Perspectives

An interactive blog sharing the Fulcrum team's policy updates and analysis.

Recommended Weekend Reads

Why We Should Ignore Bilateral Trade Balances, Hutchison’s Sprawling Portfolio of Ports in Latin America, Seven Reasons Putin Doesn’t Want to End the Ukraine War, and Putting Economics Back into Geoeconomics

April 17 - 20, 2025

Spring is here, and it’s Easter Weekend. Here are our latest recommended reads. We hope you have a wonderful Easter and a relaxing weekend. And please let us know if you or someone you know wants to be added to our distribution list.

More on the Trade War

Bilateral Trade Balances: Ignore Them Center for Strategic and International Studies

The Trump administration appears to have given up its fantastical effort to fully remake the international trade order. Although 10% tariffs versus almost everyone and 145% tariffs against China are still in place, the administration has for the time put aside the revolutionary notion of substituting reciprocal tariffs negotiated country-by-country with basing trade in commonly applied tariffs and making modest adjustments, lower or higher, in exceptional circumstances. That said, the administration is still absolutely fixated on bilateral trade deficits – that they inherently represent a deadweight loss (despite U.S. companies and households receiving goods and services in return) and that those countries with surpluses are by definition scofflaws who are guilty of stealing American manufacturing capabilities, jobs, and wealth.

A Stab at China’s View of the “Trade War” Derek Scissors/American Enterprise Institute

Rather than pretend the latest Trump administration spin on its latest walk-back is worth the time, it may be useful to assess the side that loves stability. China cares less about tariffs than it may seem. The key reason: Beijing’s prime goal isn’t prosperity, but leverage. Many experts on trade and China have recently emerged. Some were previously experts on inflation, Ukraine, and Covid. The biggest error made by newcomers is believing Xi Jinping is interested in what foreign commentators think he should be interested in—economic growth, the welfare of households, stock prices, and supposedly high American tariffs. None are especially important for Xi and, therefore, for the PRC’s policy. Economic growth is nice, it’s not close to paramount. China no longer needs fast growth to create jobs, with the labor force contracting since at least 2017. On official figures, growth is tenuously connected to job creation. This is another reason not to care much: Results will be whatever Beijing wants. China has offered decades of dubious economic statistics, eagerly repeated by many. It just happened again, with Q1 data not making arithmetic sense.

Navigating tariffs with a geopolitical nerve center McKinsey & Company

Tariffs and trade controls are expanding rapidly around the world. Macroeconomic uncertainty is growing. Second-order effects of government actions are multiplying. The first global economic shock since the COVID-19 pandemic has arrived. While geopolitical tensions have been rising for several years, the recent wave of trade controls and reciprocal tariffs has come on quickly and intensely. Not since the 1930s has the world seen this level of tariff activity.

The Americas

Surveying Hutchison’s Portfolio in Latin America: Strategic Vulnerability or Business as Usual? Center for Strategic and International Studies

China’s global network of ports has been the subject of growing anxiety among U.S. policymakers and defense analysts. Control over ports confers a host of benefits ranging from intelligence collection opportunities to access to favorable shipping lanes to even a limited power projection capability for the People’s Liberation Army Navy (PLAN). At the center of this drama is Hong Kong-based CK Hutchison, a massive conglomerate that, through its subsidiary Hutchison Port Holdings, operates the ports of Balboa and Cristobal on the Pacific and Atlantic sides of the canal, respectively. On March 4, CK Hutchison made headlines when it announced a deal with U.S. private equity firm BlackRock to buy out its port holdings outside of mainland China and Hong Kong. If executed, the deal would transfer 43 different ports across 23 countries from Hutchison to BlackRock’s control. In the Western Hemisphere alone, Hutchison currently operates seven container terminals: two in Panama, four in Mexico, and one in the Bahamas. Several of these rank among the busiest ports in the Americas and are invaluable to maritime commerce in the region.

Milei’s bold move: making Argentina’s economy normal The Economist

“Instead of talking about growth at Chinese rates, the world will soon be talking about growth at Argentine rates,” crowed Javier Milei on late-night television on April 11th. His economy minister had just outlined a $20 billion IMF program, a reduction in capital controls, and a shift to a more flexible exchange rate. He slashed spending immediately, pulling inflation sharply down. A deep recession is now giving way to strong growth. The rate of poverty, which rose to 53% of all Argentines in early 2024, has now fallen back to 38%, lower than it was when Mr. Milei took office. Now he is tackling the weakness in his reform program: capital controls and the overvalued peso. He has never been closer to transforming Argentina into a normal economy. But global economic chaos endangers his reforms, and politics could still trip him up.

Why Russia Might Reject A Peace Deal With Ukraine

Seven Reasons Putin Doesn’t Want to End the War in Ukraine Politico

Noted Russian scholar Leon Aaron lays out seven reasons Russian President Vladimir Putin does not want to end the War on Ukraine: 1) the war provides a rationale for Putin’s dictatorship, 2) Putin likes the trappings of militarism, 3) Russia’s economy now is dependent on the war, 4), Ending wartime bonuses and other perks could cause social unrest, 5) Change is destabilizing in authoritarian regimes, 6), Putin is an opportunist and a risk taker – every new concession prompts more ultimatums by Putin, and 7) Putin needs victory, not peace.

Russia’s Increasingly Bellicose Elite Center for European Policy Analysis

The economic, military, and cultural elites of wartime Russia are undergoing a transformation, and their influence on the country’s leadership does not augur a quick end to the fighting. More people with an interest in continuing the war against Ukraine are joining Vladimir Putin’s entourage, making the Kremlin even less open to peace.

Understanding the New and Old Washington

How to Make Friends and Influence POTUS MIT Sloan Management Review

The rules of corporate influence in Washington are changing dramatically. In President Donald Trump’s second term, power has shifted from Congress to the White House, turning lobbying into a personalized game of presidential access. At the same time, the use of AI tools is transforming lobbying efforts and posing ethical dilemmas. As the lobbying landscape shifts, executives must deal with the current situation with open eyes and a carefully considered strategy.

A Historical and Geographical Look at Federal Employment Levels Federal Reserve Bank of St. Louis

It’s easy to interpret the increase in the budget deficit as meaning the government itself has gotten larger. In terms of its budget and subsequent debt, that is certainly true. But in terms of the number of government employees, this isn’t quite as obvious. In the first figure, we plot federal employment from 1939 through 2024. Absent the immediate aftermath of World War II and the Korean War, there is a consistent rise in federal employment extending through the 1980s. At this point, federal employment began to decline but has largely been flat throughout much of the 2000s. Exceptions include the decennial census hirings, which lead to short-lived spikes, and a rise in federal employment starting in late 2022. Still, as a percentage of the U.S. labor force, the share of federal workers stood at around 1.8% at the end of 2024 versus 2.5% at the end of 1989.

Geoeconomics

Putting Economics Back into Geoeconomics Christopher Clayton/Mateio Maggiori/Jesse Schreger – National Bureau of Economic Research

Geoeconomics is the use of a country’s economic strength to exert influence on foreign entities to achieve geopolitical or economic goals. We discuss how concepts of power in the political science and economics literature can be used to guide research on geoeconomics. Economic threats as a form of coercion have seen a recent resurgence. We show how different types of threats can be modeled using simple tools and discuss what channels their potential effectiveness is based on. We discuss important open questions for the future literature to pursue.

Which Generation Spends More? U.S. Bureau of Labor Statistics

As it turns out, spending does differ along generational lines. In 2023 (the latest available data), those born between 1965 and 1980 spent the most, with annual household expenditures averaging $95,692. This generation was between the ages of 43 and 58 in that year and perhaps in one of the highest-earning periods of their working lives. By contrast, the lowest average expenditure was $49,206, spent by those born in in 1945 or earlier and likely retired. Average annual expenditures for all households in 2023 were $77,280, a 5.9-percent increase from 2022. During the same period, the Consumer Price Index for All Urban Consumers rose 4.1 percent, and average income before taxes increased 8.3 percent. These data are from the Consumer Expenditure Surveys program. For more information, please see the latest news release at “Consumer Expenditures – 2023,” as well as Consumer Expenditures data tables. Consumer expenditure data are averages for all consumer units (households). Consumer units consist of families, single persons living alone or sharing a household with others but who are financially independent, or two or more persons living together who share major expenses.

Recommended Weekend Reads

BRICS Expansion and What Its Members Want, The Growth of Institutionalized Fraud, Hezbollah’s Latin American Networks, and Does Putin Trust Anyone in Russia Anymore?

April 4 - 6, 2025

Here are our recommended reads from reports and articles we read in the last week. With all that has happened and been written this week on Trump’s new tariff regime, we refrained from including anything on tariffs but we are assembling a special collection of research for next week. In the meantime, we hope you find these useful and that you have a relaxing weekend. And let us know if you or someone you know wants to be added to our distribution list.

Geoconomics

BRICS Expansion and the Future of World Order: Perspectives from Member States, Partners, and Aspirants Carnegie Endowment for International Peace

Among analysts, the significance of the BRICS expansion remains a matter of debate. On paper, “BRICS+” has the potential to become a major geopolitical and geoeconomic force. The bloc already boasts about 45 percent of the world’s population, generates more than 35 percent of its GDP (as measured in purchasing power parity, or PPP), and produces 30 percent of its oil. BRICS countries have also established an extensive and thickening latticework of intergovernmental cooperation. Many analysts, therefore, depict BRICS expansion as a watershed moment in the shift to a more egalitarian international system.

Demand for College Labor in the 21st Century Federal Reserve Bank of Cleveland

Tracing the evolution of labor demand in the United States, this Economic Commentary reveals that the disproportionate rise in relative productivity of college-educated labor that shaped the latter half of the 20th century has plateaued since 2000. Our analysis suggests that technical change in the 21st century may no longer favor college graduates, in which case further growth in the employment share of college-educated workers would likely lower the premium that college-educated workers receive compared with non-college-educated workers.

Why extracting data from PDFs is still a nightmare for data experts Ars Technia

AI has one enormous challenge. For years, businesses, governments, and researchers have struggled with a persistent problem: How to extract usable data from Portable Document Format (PDF) files. These digital documents serve as containers for everything from scientific research to government records, but their rigid formats often trap the data inside, making it difficult for machines to read and analyze.

“Industrialized Fraud” Excerpt from Stripe’s Annual Letter

Stripe published their annual letter covering a host of trends the finance company is seeing transform. But there was one shocking observation – the explosive growth of institutionalized fraud: “Fraud is a bigger drag on the global economy than you might think: one report found that fraud cost 3% of a typical online business’s revenue. Fraudulent actors today operate on an industrial scale, with teams of engineers, managers, and data analysts. (We are yet to verify whether they have HR departments. If you know, please tell us so we can give them some peer feedback.) Fraudulent actors generally target times when fraud teams are offline—we see more fraud on Saturdays, Sundays, and Mondays—but we see subtler patterns, too, like the fraudsters’ own work schedules. Fraudsters are particular about their lunch breaks.”

The Psychology of Free: How a Price of Zero Influences Decision-making Federal Reserve Bank of St. Louis

Why do we get so excited when we see the word “free”? In competitive markets, businesses use strategies to attract customers and increase sales. One effective and appealing tactic is offering something for free. Examples include “Buy one, get one free!” and “Free samples inside!” The power of “free” goes beyond just saving money; it involves psychological factors that influence our decisions without us realizing it. Free items, free shipping, and the psychological impact of “free” reveal much about social norms and human decision-making.

Americas

Hezbollah's Networks in Latin America: Potential Implications for U.S. Policy and Research Rand

Most people have no idea Hezbollah operates in Latin America. Academic literature and government reports almost universally indicate that Hezbollah's activities in the region pose potential threats to U.S. national security. However, there is a significant knowledge gap in existing assessments. In this paper, the author offers an initial exploration of Hezbollah's operational footprint in Latin America, focusing on illicit funding mechanisms, violent operations, and key operational hubs — particularly in the Tri-Border Area and Venezuela. The analysis situates these activities within the broader context of Iran's regional diplomatic, economic, and cultural activities, which partially facilitate conditions amenable to Hezbollah's operations.

Assessing Guatemala as a Nearshoring Destination Center for Strategic and International Studies

Guatemala’s geographic proximity to the United States and Mexico gives it an advantage when trying to lure North American businesses seeking to shorten and strengthen their supply chain routes. The country, which has the United States as its largest trading partner, has the potential to leverage the nearshoring movement and attract businesses seeking alternative hubs to Mexico, especially as the Guatemalan government continues to make efforts to enhance its competitiveness, promote investment opportunities, and work on reforms to support economic growth.

Inside the President’s Daily Brief War Room Podcast

Ever wonder what goes into the President’s Daily Brief (PDB)? It’s not your average morning news. Stephanie Sellers, a former PDB briefer, is currently the Central Intelligence Agency (CIA) Representative to the U.S. Army War College and the General Walter Bedell Smith Chair of National Intelligence Studies. She joins host Ron Granieri to share her experiences and describes the job as trying to keep up with “17 different soap operas at once.” This crucial intelligence update is delivered to the president and other senior government leaders, shaping their understanding of critical issues. Sellers, who previously worked on missile systems for the Navy, joined the CIA after 9/11 out of a desire to continue to serve her country and to use and grow her technical and leadership skills in new and exciting assignments. Her journey to becoming a PDB briefer was fueled by a desire for challenge and the opportunity to work at “the nexus of intelligence and policy.”

Russia, China, North Korea, the US, and the Ukraine War

On a spring morning, two months after Vladimir Putin’s invading armies marched into Ukraine, a convoy of unmarked cars slid up to a Kyiv street corner and collected two middle-aged men in civilian clothes. Leaving the city, the convoy — manned by British commandos, out of uniform but heavily armed — traveled 400 miles west to the Polish border. The crossing was seamless, on diplomatic passports. Farther on, they came to the Rzeszów-Jasionka Airport, where an idling C-130 cargo plane waited. The passengers were top Ukrainian generals. Their destination was Clay Kaserne, the headquarters of U.S. Army Europe and Africa in Wiesbaden, Germany. Their mission was to help forge what would become one of the most closely guarded secrets of the war in Ukraine.

Auditing the Auditors: Does Putin Trust Anyone Now? Carnegie Politika

A new type of Russian bureaucrat has emerged in recent years: those appointed by President Vladimir Putin to oversee certain agencies or sectors and keep an eye on the officials formally in charge—even those who ostensibly enjoy the Kremlin’s trust. These “auditors” can now be found everywhere: from the Russian delegation conducting negotiations with the United States to the Defense Ministry, the Emergencies Ministry, and the presidential administration. While these appointments help to reassure Putin that he remains in control, they also threaten to undermine the viability of Russia’s power vertical. It’s recently become clear, however, that the president does not trust even long-serving officials and has decided to create a new tier of bureaucracy to oversee them.

Can Trump Channel Nixon to Turn Russia Against China? Carnegie Politika

The Trump administration has been quite open about why exactly it wants to get into bed with Moscow: it believes closer ties will prize Russia away from China, which it sees as the real existential threat to the United States. A previous U.S. president—Richard Nixon—came up with a similar plan at the beginning of the 1970s. The only difference is that Nixon’s plan was supposed to work the other way around: improving relations with China to isolate the Soviet Union. Back then, the U.S. strategy worked—more or less. Donald Trump’s modern-day imitation of Nixon, however, is unlikely to succeed.

China and Russia’s strategic relationship amid a shifting geopolitical landscape Brookings Institution Commentary

The geopolitical landscape is shifting at a breakneck pace, raising urgent questions about how the China-Russia strategic relationship—both with each other and with the United States—might evolve, and what this means for the war in Ukraine and the broader global order. In the conversation that follows, four experts—Aslı Aydıntaşbaş, Angela Stent, Tara Varma, and Ali Wyne—join Patricia Kim to unpack these critical developments. They explore topics ranging from the consequences of a potential U.S.-Russia reset or a “reverse Nixon” strategy, to China’s evolving strategic calculus, the future of the China-Russia-North Korea-Iran “axis,” and Europe’s uncertain path forward. Join us as we delve into what’s at stake for Washington, Beijing, and the world.

Russia-China-North Korea Relations: Obstacles to a Trilateral Axis Foreign Policy Research Institute

This paper begins by examining the history of Russia-China-North Korea interactions, highlighting Sino-Russian differences in emphasis regarding North Korea prior to the full-scale war in Ukraine. To assess whether a trilateral axis formed after 2022, the paper examines evidence of institutionalized cooperation, coordination of Chinese and North Korean military aid to Russia for Ukraine, and Russian and Chinese expert perspectives. The paper then addresses the obstacles to the formation of a trilateral axis. Although authoritarian states share an overriding interest in regime security and political survival, this does not necessarily mean that we should expect solidarity among similarly disposed regimes or believe that they would inevitably form an anti-Western axis. Considerable research has been done on the reasons why authoritarian states choose to support one another, but it is important to understand what factors might limit their cooperation. This paper examines how the historical experience of trilateralism, reputational concerns, foreign policy considerations, and domestic factors make a new China-Russia-North Korea axis unlikely.

Recommended Weekend Reads

Guides to Understanding Trump’s Trade and Foreign Policy, What the EU Must Do to Build Up Their Defense Capabilities, the US Workforce Challenge, and Why China Isn’t the Obvious Winner in Latin America

March 28 - 30, 2025

Understanding Trump's Trade and Foreign Policy

A User’s Guide to Restructuring the Global Trading System Stephen Miran/Hudson Bay Capital

Stephen Miran is one of President Donald Trump’s top economic advisors. He chairs the White house Council of Economic Advisors. He is also the author of a 41-page memo – more a blueprint - that lays out what can be achieved by what is being billed as a “Mar-A-Lago Accord” which would revise the framework for the global financial system.

Trump, Strategy, and Mercantilism School of War Podcast

Walter Russell Mead, Alexander Hamilton Professor of Strategy and Statecraft at the University of Florida's Hamilton Center and columnist for The Wall Street Journal, joins the show to talk about the role of economic issues in Trump’s strategic views. They discuss Mercantilism and physiocracy, the role of Silicon Valley, the dollar, coalitions, tariffs, China, and what President Trump thinks about all of it.

Annual Threat Assessment of the U.S. Intelligence Community Office of the Director of National Intelligence

In this year’s public annual report – the first of the new Trump Administration and under the oversight of new DNI Tulsi Gabbard- the DNI points out the following: Both state and nonstate actors pose multiple immediate threats to the Homeland and U.S. national interests. Terrorist and transnational criminal organizations are directly threatening our citizens. Cartels are largely responsible for the more than 52,000 U.S. deaths from synthetic opioids in the 12 months ending in October 2024 and helped facilitate the nearly three million illegal migrant arrivals in 2024, straining resources and putting U.S. communities at risk. A range of cyber and intelligence actors are targeting our wealth, critical infrastructure, telecom, and media. Nonstate groups are often enabled, both directly and indirectly, by state actors, such as China and India as sources of precursors and equipment for drug traffickers. State adversaries have weapons that can strike U.S. territory, or disable vital U.S. systems in space, for coercive aims or actual war. These threats reinforce each other, creating a vastly more complex and dangerous security environment. Russia, China, Iran and North Korea—individually and collectively—are challenging U.S. interests in the world by attacking or threatening others in their regions, with both asymmetric and conventional hard power tactics, and promoting alternative systems to compete with the United States, primarily in trade, finance, and security.

The EU’s Move to Build Up Its Defense Capabilities

Joint White Paper for European Defense Readiness 2030 European Commission

From the paper’s introduction: The international order is undergoing changes of a magnitude not seen since 1945. These changes are particularly profound in Europe because of its central role in the major geopolitical challenges of the last century. The political equilibrium that emerged from the end of the Second World War and then the conclusion of the Cold War has been severely disrupted. However much we may be wistful about this old era, we need to accept the reality that it is not coming back. Upholding the international rules-based order will remain of utmost importance, both in our interest and as an expression of our values. However, a new international order will be formed in the second half of this decade and beyond. Unless we shape this order – in both our region and beyond – we will be passive recipients of the outcome of this period of interstate competition with all the negative consequences that could flow from this, including the real prospect of full-scale war. History will not forgive us for inaction.

Defending Europe without the US: first estimates of what is needed A Joint Publication of Bruegel and the Kiel Institute for the World Economy

Europe could need 300,000 more troops and an annual defense spending hike of at least €250 billion in the short term to deter Russian aggression. From a macroeconomic perspective, a debt-funded increase in defense spending should boost European economic activity at a time when external demand may be undermined by the upcoming trade war (Ilzetzki, 2025; Ramey, 2011), though yields and inflation may rise. Ilzetzki (2025) argued that defense spending can also positively contribute to long-term growth via innovation, but a precise quantification of such effects is still needed.

The Case for Europe Strategic Europe

By choosing to vote against a United Nations resolution marking the third anniversary of Russia’s invasion of Ukraine, the United States seems intent on abandoning its leadership of the West after eighty years of hegemony. Europe is going through its gravest hour since the Second World War—and most Transatlanticist political leaders are starting to realize it. At best, Europe will have to defend its territory alone and take responsibility for deterrence. At worst, it will have to fend off great powers actively seeking to subvert it as they assert their respective spheres of influence. This could involve political interference, economic coercion, and open aggression, tearing Europe apart. Europe’s choice lies in between these two scenarios. Rather than predict success or failure, it is worth outlining the building blocks that make the case for a stronger Europe possible and the pitfalls this vision could run into.

Germany’s big spending splurge gives EU the jitters Politico Europe

European Union governments have expressed fears that the radical spending plans announced by Germany’s chancellor-in-waiting will end up skewing the bloc’s single market and could give the country an unfair competitive edge. A month on from an election that made Friedrich Merz almost certainly the next leader in Berlin, the upper house of parliament on Friday approved a historic change to the country's basic law to exclude defense investment above 1 percent of economic output from the nation’s strict spending rules, along with a €500 billion fund for infrastructure and green energy, clearing the final parliamentary hurdle. While Germany’s allies in Europe have broadly welcomed Berlin’s long-awaited loosening of the purse strings, there is a sense of unease about the impact it could have at a time when economies are still struggling to recover after the twin shocks of Covid and the Ukraine conflict, and with the looming threat of a trade war with the U.S.

Why Europe can’t defend itself: Political fragmentation is blocking autonomy Wolfgang Munchau/UnHerd

Imagine a world in which Western Europe was actually able to stick it to Vladimir Putin and Donald Trump simultaneously. As if. Back in the real world, there’s a remote possibility the Europeans might get their act together sufficiently to stand up to one, or the other. But not both. They will, in classic fashion, be split. Some of the eastern European countries, the Baltic States, for example, will prioritize a push-back against Russia. Others, like France, are more concerned with driving their independence from the US. Then there is a third group that wants neither. So, where does that leave Europe? What they are agreed on is the plan is to increase military spending. The EU will follow Germany’s example and partially exempt the defense budget from the fiscal rules. But the truth is, no amount of investment will wean the EU off its American dependency any time soon. It will take decades to close the immense defense technology gap. To build entire industries from scratch takes time. You need defense companies, supply chains, and know-how. Europe is far from the cutting edge of 21st century defense technology and its expertise in that sector has been diminished since the end of the Cold War.

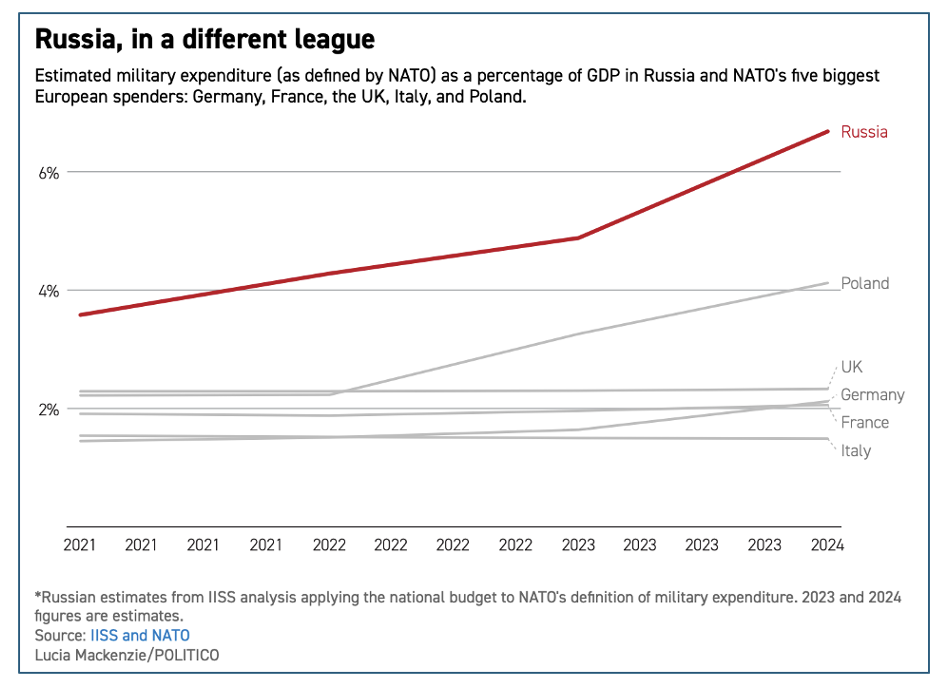

Behind NATO’s 2 Percent: Measuring the True Scope of Alliance Defense Investments and the NATO Defense Deficit Mackenzie Eaglen & Cole Spiller/American Enterprise Institute

This working paper examines NATO’s military spending through two key lenses: how NATO allies measure defense expenditures and the strategic implications of the long-term defense deficit created by chronic underfunding. While 21 member states now meet the 2 percent of GDP benchmark, the alliance must look beyond numerical targets to assess whether these investments translate into real military capability.2 Closing NATO’s $2 trillion defense deficit requires greater transparency in accounting to allow for more complete analysis, as well as sustained increases in spending to build credible deterrence against rising threats.

The Changing US Workforce

Shifting Immigration Toward High-Skilled Workers Penn Wharton Budget Model

We evaluate two immigration policies that shift 10 percent of future low-skilled immigration toward either: (i) high-skilled immigrants (“HSI”) that otherwise maintains the current share of STEM workers within the high-skilled group, or (ii) only high-skilled STEM workers (“HSI STEM”) that increases the share of STEM relative to other high-skill workers. The number of total immigrants remains the same under both policies. Both policies grow the economy, reduce federal debt, and increase wages across all income groups: lower-skilled, higher-skilled non-STEM workers, and higher-skilled STEM workers. In fact, this policy change affords the rare opportunity of a “Pareto improvement” benefitting all groups.

Technology Adoption and the Changing Role and Background of Clerical Workers Federal Reserve Bank of Cleveland

From 1980 through 2015, the share of clerical jobs in the employed labor force declined more significantly in large and expensive cities than in smaller cities. Moreover, the remaining workers performing these occupations in large and expensive cities had, on average, higher education levels and were more likely to perform tasks usually done by managerial and professional personnel when compared to their small-city counterparts. In this Economic Commentary, we show how these patterns are related to the uneven adoption of information communication technologies (ICT) across geographies and discuss adoption’s impact on clerical jobs’ tasks and worker requirements.

Defensive Hiring and Creative Destruction Jesus Fernandez-Villaverde/Yang Yu/Francesco Zanetti/National Bureau of Economic Research

America has long struggled with a lack of productivity growth despite huge investment in research and development. Jesús Fernández-Villaverde, Yang Yu, and Francesco Zanetti find that the defensive hiring of researchers by incumbent firms with monopsony power reduces creative destruction, which in turn maintains the status quo and leads to stagnant productivity growth.

The Americas

China Won’t Be the Obvious Winner in Latin America Ryan Berg/Foreign Policy

After a mere two months in office, a narrative on the Trump administration’s policy toward LAC and great-power competition has emerged: Regional influence will accrue to China at the expense of the United States because Washington appears a “bully,” has talked of reviving the controversial Monroe Doctrine, and has occasionally adopted the rhetoric of territorial expansion. A deputy assistant secretary of state in the Biden administration accused the Trump administration of shortsightedness, leading to “an opening for China, made in America.” Even a former staffer in the first Trump administration worried that the current approach to LAC “could unwittingly facilitate the extension of Beijing’s influence.” Will the Trump administration’s more assertive approach toward LAC benefit China?

What Elections Mean for Canada and the Future of North America Center for Strategic and International Studies

On March 23, newly minted Canadian Prime Minister Mark Carney announced snap elections for April 28, kicking off a contest to determine Canada’s future at a critical juncture. The election pits the incumbent Liberal Party, which has received a second wind since January in part due to tariffs and political threats from the United States, against the Conservative Party under the leadership of “Canada First” politician Pierre Poilievre. No matter the outcome, however, the next leader of Canada will inherit a tense relationship with the United States, public pressure to deliver economic gains, and an increasingly fraught global security environment that impinges upon Canada’s sovereignty.

Recommended Weekend Reads

The War on Ukraine, Broader Implications of the Peace Talks, Argentina’s Big Challenge, and the Future of Europe’s Security

March 14 - 16, 2025

Russia’s War on Ukraine and The Implications of a Possible Cease Fire

The Kremlin's Balancing Act Foreign Policy Research Institute

Following Russia’s invasion of Ukraine, the Russian government accelerated the preexisting trend of centralizing control over regional power and economic assets. This study explains the shift of government control, highlights instances of pushback, and identifies limitations on the Kremlin's strategy going forward. The Kremlin's centralization drive has manifested in several ways, including tightening control over regional and municipal political institutions, expanding financial control over regional budgets and policy priorities, nationalizing and indirectly mobilizing business assets, and introducing new priorities in personnel policy. These changes have created winners and losers, resulting in friction and resistance from regional elites who perceive their interests and autonomy as threatened. The sustainability of the Kremlin's strategy is uncertain and risks intensifying tensions and worsening government instability.

Lessons from Minsk II for the Ukraine peace talks Brussels Signal

The road to peace in Ukraine is extremely difficult and perhaps also very long, despite President Trump’s initial hopes. Even agreeing an initial ceasefire in Ukraine is a tall order, as this Tuesday’s Trump-Putin phone call attests. Nonetheless, negotiations will continue, particularly as all sides – Ukraine, Russia and the US – appear committed to achieving a full peace agreement rather than merely a Korean-style ceasefire. Yet a full peace treaty is much more considerable undertaking, and these negotiations remain overshadowed by the failure of the Minsk II Agreement – a 2015 diplomatic effort that promised peace but ultimately collapsed. The lessons of Minsk II offer sobering insights into the obstacles facing any new settlement and the structural flaws that must be avoided if a sustainable resolution is to be achieved.

Russia’s Peace Demands on Ukraine Have Not Budged Council on Foreign Relations

President Trump, in his recent address to Congress, said Russia has sent “strong signals that they are ready for peace.” Is that true? Not really. The Kremlin has not budged from its maximal demands for ending the conflict, which Russian President Vladimir Putin laid out last June and includes:

No NATO membership for Ukraine;

Ukraine’s recognition of Russia’s annexation of four Ukrainian provinces (even though Russia does not physically control all the territory of three of them);

Ukraine’s demilitarization and denazification (code for the installation of a pro-Russia puppet in Kyiv); and

the lifting of anti-Russia sanctions.

During a visit to the Defenders of the Fatherland Foundation, Putin doubled down on that position just last week, saying that Russia does not intend to make any compromises in peace negotiations. The Russian president sees no need to make any concessions. His armies are making grinding progress on the battlefield, albeit at a heavy cost in men and materiel. The Russian economy has proven resilient to Western sanctions, growing by more than 4 percent each of the past two years. Ukraine, meanwhile, is facing severe manpower shortages, and Western support is flagging.

Turkey in a Trump-and-Putin World Carnegie Endowment for International Peace

The disruptions to the world order caused by Russia and the new U.S. administration complicate Turkey’s balancing act between Moscow and the West. But these shifts could offer Ankara a chance to shape the evolving security dynamics and contribute to Europe’s stability. Yet Turkish President Recep Tayyip Erdoğan cracked down on Turkish opposition parties this past week, arresting dozens of politicians, fearful of losing power in the upcoming elections and exposing the fragility of his government.

A Blueprint for a European Defense Force Strategic Europe

As the U.S. commitment to Europe’s security wanes and Russia’s threat to the continent grows, the need for a European defense force is becoming more pressing than ever. By expanding existing frameworks and investing in Ukraine’s defense industry, Europe can begin to take charge of its own security.

The Tariff Wars

The Incoherent Case for Tariffs Chad Brown/Douglas Irwin – Foreign Affairs Magazine

Less than two months into his second term, U.S. President Donald Trump has made good—with startling intensity—on his campaign promise to impose tariffs. On inauguration day, he issued the America First Trade Policy Memorandum to review U.S. trade policy with an eye toward a new tariff regime. Over the first two weeks of February, he set in motion new duties covering nearly half a trillion dollars of U.S. imports. On March 4, he doubled the size of his already significant February tariff increase on China. Over this period, he has also announced, suspended, announced again, and suspended again 25 percent tariffs on goods from Canada and Mexico. And his administration has pledged to impose reciprocal tariffs on April 2. The result has been uncertainty, chaos, and immediate retaliation from some of the United States’ biggest trade partners. All this economic upheaval raises a central question: Why is Trump so focused on tariffs?

Trump’s tariffs challenge India’s economic balance The Australian Strategic Policy Institute

US President Donald Trump’s tariff threats have dominated headlines in India in recent weeks. Earlier this month, Trump announced that his reciprocal tariffs—matching other countries’ tariffs on American goods—will go into effect on 2 April, causing Indian exporters to panic at the prospect of being embroiled in Trump’s escalating trade war. The economic impact on India, which runs a trade surplus with the US, could be significant. India exported goods worth nearly $74 billion to the US in 2024, and estimates suggest that Trump’s new tariffs could cost the country up to $7 billion annually. But the implications could be much more far-reaching. One analysis estimates that India effectively imposes a 9.5 percent tariff on US goods, while US levies on Indian imports are only 3 percent. If Trump follows through on his pledge of full tariff reciprocity, that imbalance will vanish—along with the cost advantages many Indian exporters currently enjoy.

Antitrust Fuels Trade Tensions CEPA

President Donald Trump’s tariff threats target “discrimination against American innovation,” and US legislators point to the EU’s Digital Markets Act as evidence – even as the US pursues its own tech antitrust cases. The tensions underline a troubling reality: antitrust enforcement has become politicized, and as the Paris-based OECD Club of advanced democracies has long recognized, the politicization of antitrust enforcement makes markets less dynamic, less competitive, and less efficient, ultimately harming consumers. This outcome can be avoided if both European and American leaders depoliticize and focus enforcement on making markets work for consumers.

The Optimal Monetary Policy Response to Tariffs Javier Bianchi & Louphou Coulibaly/NBER

What is the optimal monetary policy response to tariffs? This paper explores this question within an open-economy New Keynesian model and shows that the optimal monetary policy response is expansionary, with inflation rising above and beyond the direct effects of tariffs. This result holds regardless of whether tariffs apply to consumption goods or intermediate inputs, whether the shock is temporary or permanent, and whether tariffs address other distortions.

Geoeconomics

Should Friday be the New Saturday? Hours Worked and Hours Wanted National Bureau of Economic Research

This paper investigates self-reported wedges between how much people work and how much they want to work at their current wage. More than two-thirds of full-time workers in German survey data are overworked—actual hours exceed desired hours. We combine this evidence with a simple labor supply model to assess the welfare consequences of tighter weekly hours limits via willingness-to-pay calculations. According to counterfactuals, the optimal length of the workweek in Germany is 37 hours. Introducing such a cap would raise welfare by .8-1.6% of GDP. The gains from a shortened workweek are largest for workers who are married, female, white collar, middle-aged, and high-income. An extended analysis integrates a non-constant wage-hours relationship, falling capital returns, and a shrinking tax base.

Around 60% of the fixed-rate debt in the OECD that will mature by 2027 (approximately $9T) was issued in 2021 or earlier, before the recent tightening cycle, most likely at yields below current market rates. The weighted average YTM of the maturing debt in 2025-27 remains below 2% in all three years, [while] the average of the projected 10-year interest rate in OECD countries is expected to remain around 3.6% in 2025. The debt maturing in 2025-27 will, therefore, likely be refinanced at nearly twice the original rates. Increased borrowing needs and high borrowing costs have driven interest payments to a higher share of GDP in 2024, [contributing to] the first increase in the central government marketable debt-to-GDP ratio since 2020. The supply of bonds needing to be absorbed by the market accelerated as central banks continued to scale back their holdings. Four countries — France, Spain, the United Kingdom, and the United States — face heightened vulnerability, with the debt maturing by 2027 exceeding 15% of their current GDP and the average yield-to-maturity on debt issued in 2024 surpassing that of this maturing debt by over 1.5 percentage points.

Africa and Critical Minerals

·Zimbabwe’s lithium beneficiation policy: a catalyst for Vision 2030 ISS/Africa Futures

As the global green energy transition gains momentum, lithium has emerged as the new gold, particularly in the automotive industry, due to its essential role in lithium-ion batteries. The demand for lithium continues to soar, and Zimbabwe stands at a competitive advantage as home to Africa’s largest lithium reserves and ranking among the world's top five in estimated deposits. If managed effectively, lithium beneficiation can drive Zimbabwe towards achieving its Vision 2030, transforming the country into an upper-middle-income economy. A fundamental aspect of this ambitious goal is attaining a GDP growth rate of 8–9% by 2030.

Can the DRC Leverage U.S.-China Competition Over Critical Minerals for Peace? Carnegie Endowment for International Peace

The Democratic Republic of the Congo (DRC) is offering the United States access to its mineral resources in an effort to ensure peace and stability in the country. The offer, made against the backdrop of U.S.-China competition over critical minerals, is designed to motivate Washington to play a decisive role in the security crisis in the eastern DRC. Unlike in 2012, when then-president Barack Obama threw his weight into pressuring Rwanda to halt its support for the M23 (March 23) rebel movement, more recent U.S. administrations, past and current, have struggled to play a decisive role in the conflict raging in the eastern DRC, where the Congolese government is battling Rwandan-backed M23/AFC (Alliance Fleuve Congo) rebels.

Latin America

Chevron Out, Black Market In? The Fallout of U.S. Sanctions on Venezuela Oilprice.com

On February 26, President Trump announced his intention to end General License 41, which allowed Chevron to operate in Venezuela despite sanctions. The U.S. Treasury’s Office of Foreign Assets Control (OFAC) had created a system to monitor at least part of Venezuela’s oil industry by waiving sanctions for certain American, European, and Indian companies but with strict limitations. Four corporations that were authorized by licenses or comfort letters—Chevron, Repsol, Maurel et Prom, and Eni—contributed to a production of 325,000 barrels per day (bpd) in January, to the country’s total of 1,068,000 bpd, according to PDVSA, the state-owned energy company. The big question now is will it spur a massive rise of black-market oil coming out of Venezuela?

A Key Pending Challenge for Milei’s Argentina Americas Quarterly

Argentine President Javier Milei campaigned on two key promises: To bring the country’s high and accelerating inflation to a halt by dollarizing the economy and closing down the Argentine central bank (BCRA) and to balance the budget by taking a chainsaw to wasteful government spending. Now, 15 months into his term in office, he has made heroic progress on the fiscal and inflation fronts. But by forsaking dollarization and keeping currency and capital controls in place, Milei has jeopardized his anti-inflationary program and discouraged a potential investment boom.

North Korea

The North Korean tourist trap The interpreter/Lowry Institute

Having closed the country even more tightly during the Covid pandemic, last month, North Korea put out the welcome sign for a small group of foreign tourists from Australia, the United Kingdom, France, Germany, and Canada for the first time since 2020. Yet the gates slammed shut again last week when Pyongyang announced it would grant no new tourism visas. Visitors from Russia have been allowed in since February 2024, but Chinese nationals, once North Korea’s main source of foreign tourists, have still not returned. The abrupt closure raised eyebrows, considering that North Korea’s Kim Jong-un has invested in key tourism facilities in Mount Chilbo, Mount Paektu, Mount Kumgang, and the Wonsan-Kalma resort area in preparation for the post-lockdown rebound in foreign visitors.

Recommended Weekend Reads

Business Strategy in a New Geopolitical Age, Chile’s Libertarian Presidential Candidate, One Moment and Two Speeches, Data Center Energy Demands, and What is the Mar-a-Lago Accord?

March 14 - 16, 2025

Below are our recommended reads from reports and articles we read in the last week. We hope you find these useful and that you have a relaxing weekend. And let us know if you or someone you know wants to be added to our distribution list.

Business Strategy in an Age of Heightened Geopolitical Risk

How to Strategize in an Out-of-Control World MIT Sloan Management Review

During the past few years, company strategies have been disrupted repeatedly by major shocks like the COVID-19 pandemic, the outbreak of war in Ukraine and the Middle East, and breakthroughs in generative AI. In the first months of 2025, a stream of political surprises has been impacting company agendas — and further upheavals seem likely. This turbulence is having a real impact on business: Our analysis of nearly 7,000 organizations over a 20-year time frame shows that variance in company profitability can increasingly be attributed to factors that lie beyond the company and its industry. (See “What Shapes Profitability?”) Contextual factors — like geopolitics, technology, and climate — now account for 43% of the variation in the net profit margins of public corporations.

The Indo-Pacific

Conversations: China’s Naval Flotilla and Australia’s Response Lowry Institute Podcast

Defence analyst Marcus Hellyer talks with the Lowy Institute’s Sam Roggeveen about the unprecedented appearance of Chinese warships off Australia’s east coast. What message was Beijing sending? How well did Australia’s defense force perform in response? And what are Australia‘s future options with the United States in retrenchment?

One Moment, Two Speeches Center for Strategic and International Studies

Two weeks ago, the world’s two most powerful countries witnessed a rare moment of symmetry. On March 4th at 9:00 pm US EST, President Donald Trump strode into the Capitol to give his second administration’s first address to a joint session of Congress. Meanwhile, on the other side of the planet, at 9:00 am Beijing time, Chinese Premier Li Qiang was just finishing up his speech summarizing the annual Government Work Report(GWR) to the National People’s Congress. Both are two countries’ key national annual addresses in which the executive reports on the state of the country to the legislative branch. This side-by-side moment highlights not only major differences in the political systems and political theater, but also some surprising similarities in substance as well.

Trump-ism and East Asia Global Policy/Durham University

Alastair Newton argues that Donald Trump’s abandonment of the US-led international order and efforts to reshape global trade and finance do not bode well for economies in East Asia which may find themselves forced by Washington into a Chinese sphere of influence as part of a grand bargain with Beijing.

Latin America

The Radical Libertarian Reshaping Chile’s Presidential Race Americas Quarterly

He’s been called the “Gabriel Boric of the right”—maybe because, like Chile’s young president, he wears a beard and made a name for himself criticizing the country’s political establishment. But Johannes Maximilian Kaiser Barents-von Hohenhagen, 49, objects to the comparison.“ Kaiser, who proudly describes himself as a “reactionary,” is now taking a turn in the spotlight after a recent poll showed him tied for the lead in October’s presidential election. He is the latest right-wing populist in Latin America to channel widespread frustration with crime, immigration and politics as usual, although his story has some distinctly Chilean twists.

Inside a Mexican Cartel ‘Extermination’ Camp: Ovens, Shoes, and Teeth Washington Post

For months, the tips had been appearing on a Facebook page. There was a mass grave hidden in a rural village outside Guadalajara, in western Mexico, the messages said. Mexico has grappled for years with a crisis of disappearances, with more than 110,000 people reported missing. Relatives of the disappeared have unearthed hundreds of graves filled with corpses. This seemed like another. But the people who ran the Facebook page — a group in Jalisco state who search for the missing — were puzzled. After getting more anonymous tips, Indira Navarro, head of the group, and dozens of other victims’ relatives arrived on March 5 at an abandoned ranch outside La Estanzuela and started poking around. They dug up three underground ovens. They found hundreds and hundreds of singed bone shards — from skulls, fingers, teeth. It was what Mexicans call an “extermination camp.” But the image that’s really stunned Mexicans was of the shoes. There were piles of them — well over 200. The camp is a sign of how much criminal groups have penetrated the Mexican economy. They don’t just traffic drugs to the United States; they extort businesses, “tax” migrant smugglers, and run vast networks of contraband goods, from gasoline to wood. Navarro’s group believes the ranch in La Estanzuela was a recruiting and training center for one such crime group. The area is dominated by one of the country’s largest cartels, Jalisco New Generation (CJNG).

American’s View of Currencies

Cryptocurrency Ownership among U.S. Households Federal Reserve Bank of St. Louis

Cryptocurrency has become more prevalent since it first entered the global economy. However, no consistent measurement of cryptocurrency ownership among American households has emerged. This blog post uses what data are available through the Survey of Consumer Finances (SCF) to estimate the distribution of cryptocurrency ownership in the U.S., finding that roughly 4.3% of Americans held such assets.

Thoughts for Your Penny? Hoover Institution

One of the concepts you come across in a well-taught monetary economics course is the idea of seigniorage. An online dictionary does a pretty decent job of defining it: “The profit made by a government by issuing currency, especially the difference between the face value of coins and their production cost.” Although the definition highlights coins, the concept applies to paper money also. The US government makes a pretty penny (pun intended) on seigniorage. It’s not as much as it used to be because more and more people use credit cards and even cryptocurrency to buy goods and services. Still, it’s a good amount. The biggest gain from seigniorage is on the $100 bill. Printing one costs the federal government just 9.4 cents.

So, when the feds spend this $100, they make a nice profit of $99.90. Not bad. Printing a $1 bill costs the feds 3.2 cents. So even on a $1 bill, the feds make 97 cents. But minting small coins loses money for the feds. In its 2024 Annual Report, the US Mint reports the cost of producing each coin denomination. The cost of producing a penny was $0.03. In other words, the cost of producing a penny was three times the value of the penny. Interestingly, the feds went underwater even on the nickel, whose cost, at $0.11, was over twice the value of the nickel. That’s why I stated earlier that the federal government should stop producing nickels also. It isn’t until you get to the dime that you find a coin that the feds make money on. Interestingly, the cost of producing a dime, at $0.045, is less than the cost of producing a nickel.

the Race for Critical Minerals and the Growing Electrical Demand for Data Centers

Who is Paying for all that data center power? Volts Podcast/Substack

In this episode, Harvard Law's Eliza Martin and Ari Peskoe unpack how data centers' skyrocketing electricity demand could leave ordinary customers subsidizing Big Tech's power bills. Most chilling is the potential alliance between utilities and tech giants that threatens to derail much-needed utility reforms while entrenching fossil-fueled infrastructure.

The Potential for Geothermal Energy to Meet Growing Data Center Electricity Demand Rhodium Group

Next-generation geothermal energy has a number of advantages in meeting growing electricity demand from data centers. This report estimates how much of this demand could potentially be served by geothermal over the next decade.

Why the U.S. Keeps Losing to China in the Battle Over Critical Minerals Wall Street Journal

The U.S.’s desperate need for critical minerals—which include resources such as nickel, lithium and cobalt in addition to graphite—has been underscored by the Trump administration’s aggressive push for greater access in Ukraine and Greenland, rattling allies. In December, Beijing said it would ban certain mineral exports to the U.S. and conduct stricter reviews of graphite sales, in response to U.S. restrictions on semiconductor exports to China. Yet with its thumb on many of the best resources, China can dictate prices. Washington’s policy flip-flops keep blowing up miners’ plans. And many Western mining companies struggle to navigate higher-risk countries where critical minerals—all needed for green technologies and national defense—are prevalent, leaving them flat-footed when unrest erupts.

The Mar-a-Lago Accord: What Is It? Will It Happen?

What is the Mar-A-Lago Accord? Apollo Academy/Apollo Capital Management

The always brilliant Torsten Slok explains is brilliantly: The US dollar is the global reserve currency because America is the most dynamic economy in the world, and the US provides stability and security. As a result, there is upward pressure on the US dollar because everyone wants to own the world’s safest asset. This safe-haven upward pressure on the dollar overwhelms the negative impact on the dollar coming from the US current account deficit. With safe asset flows putting constant upward pressure on the dollar, there is a need for a deal—a Mar-a-Lago Accord—to put downward pressure on the US dollar to increase US exports and bring manufacturing jobs back to the US. The Mar-a-Largo Accord is the idea that the US will give the G7, the Middle East, and Latin America security and access to US markets, and in return, these countries agree to intervene to depreciate the US dollar, grow the size of the US manufacturing sector, and solve the US fiscal debt problems by swapping existing US government debt with new US Treasury century bonds. In short, the idea is that the US provides the world with security, and in return, the rest of the world helps push the dollar down in order to grow the US manufacturing sector

Meeting in Mar-a-Lago: is a New Currency Deal Plausable? Atlantic Council

In 1985, finance ministers from France, Germany, Japan, the United Kingdom, and the United States came to an agreement in the Plaza Hotel in New York City to intentionally devalue the US dollar. In the five years leading up to the Plaza Accord, the US dollar had doubled in value, threatening to upend global trade and destabilize the international financial system. Today, Washington is once again chattering about the possibility of a currency deal. This time, the venue may move south for what Trump’s incoming chairman of the Council of Economic Advisers, Stephen Miran, described as a “Mar-a-Lago Accord.” In a September report, Miran declared the overvaluation of the US dollar responsible for the “roots of economic discontent.”

Mar-a-Lago Accord, Schmar-a-Lago Accord Steven Kamin/Mark Sobel/Financial Times

In recent weeks, the buzz has been mounting about a new American plan — a “Mar a Lago Accord” — to upend the global monetary system. We can only hope it remains idle chatter. In brief, based on a detailed discussion paper by CEA Chair nominee Stephen Miran, the accord would have America’s trading partners help weaken the dollar and commit to providing low-cost, long-term financing to the US government, enforced by the threat of higher tariffs or removal of security guarantees. Intriguingly, there has been no announcement by the Trump administration or even a tweet by Trump, but Miran’s paper — along with various utterances by Treasury Secretary Scott Bessent — have led Wall Street observers to believe such an initiative is indeed in the offing. And that’s too bad, because a Mar-a-Lago Accord would be pointless, ineffectual, destabilizing, and only lead to the erosion of the dollar’s pre-eminent role in the global financial system.

Recommended Weekend Read

The Long-Run Consequences of Sanctions on Russia, North Korea’s High Casualty Learning Curve, Economic Security and Industrial Policy, and Real-Life Grand Theft Auto

February 28 - March 2, 2025

The Ukraine War

Long-Run Consequences of Sanctions on Russia David Baqaee & Hannes Malmberg / National Bureau of Economic Research

This paper examines the long-run economic consequences of Western sanctions on Russia. Using a new framework for balanced growth path analysis, we find that the long-run declines in consumption are significantly larger when capital stocks are allowed to adjust --- 1.4 times larger for Russia and 2.2 times larger for Eastern Europe. This is contrary to the common intuition that long-run effects should be milder due to greater adjustment opportunities. In our model, Russian long-run consumption falls by 8.5%, Eastern European consumption by 2%, and Western countries' consumption by 0.3% in response to sanctions. The model also reveals important distributional effects: as capital adjusts, Russian real wages fall more than rental prices in the long run. These findings show that accounting for capital adjustment is quantitatively important when analyzing trade sanctions.

The Ukraine Reparation Loan Solution Hugo Dixon & Lee Buchheit/American Enterprise Institute

Vladimir Putin will not agree to a reasonable ceasefire with Ukraine so long as he believes he will win a war of attrition. Making sure that Ukraine has a war chest to outlast Russia is therefore key to getting it a good deal. Given America’s unwillingness to continue funding Ukraine and Europe’s fiscal constraints, the best source of cash is Russia’s $300 billion in frozen assets, the lion’s share of which is in Europe. The “reparation loan” idea is an innovative way to mobilize these funds for Kyiv’s benefit without confiscating them. Europe, which balked at the reparation loan idea of outright seizure, is warming to the idea. If European governments back this plan, it will help get them a seat at the peace talks that Donald Trump has started. Threatening to use the assets in this way will give Ukraine and its allies leverage in negotiations with Russia—and will be part of a back-up plan if Putin refuses a reasonable deal.

North Korea’s Military Intervention in Kursk: A High Casualty Learning Curve 38 North

On February 8, North Korea’s (Democratic People’s Republic of Korea or DPRK) Supreme Leader Kim Jong Un issued his strongest statement of support yet for Russia’s invasion of Ukraine. While it appears as if North Korea is staying the course, its military performance thus far should give it room for pause. During the first three months after their arrival in October 2024, North Korea lost 40 percent of its 11,000-strong force contingent. An estimated 1,000 of those troops perished while 3,000 more were too severely injured to continue fighting. North Korea’s heavy casualties can be attributed to their unfamiliarity with high-intensity frontline combat, technological shortcomings and morale crises. Despite this troika of countervailing forces, North Korea’s security partnership with Russia will likely continue to strengthen.

The Maritime War in Ukraine: The Limits of Russian Sea Control? The Hague Centre for Strategic Studies

At the start of the Russian full-scale invasion of Ukraine in February 2022, the primary maritime basins of the war were under the firm grip of the advancing force. Throughout the previous decade, Russian authorities had sought to reaffirm the country’s sea control in the Black Sea and the Sea of Azov. But by November 2024, Ukrainian forces estimated Russian naval losses to include 28 warships and small boats, and one submarine. How did this reversal of fortunes happen? Russia had overwhelming capabilities and was fighting against a country with virtually no navy to speak of. How did Russia lose the battle for sea control?

Geoeconomics

Beyond the Data: China’s Economy with Leland Miller China Considered Podcast with Elizabeth Economy

In a wide-ranging conversation, Dr. Elizabeth Economy and Leland Miller talk about his experiences running China Beige Book, his insights on the Chinese economy, and conclude with a discussion about the Trump Administration’s trade policy. Miller discusses the early skepticism surrounding the China Beige Book and the process of transforming it into a valuable tool that gathers data from across the Chinese economy while serving as an independent “check” to the Chinese government. He provides insight into the methodology used, from conducting thousands of surveys within China, to looking at labor, manufacturing, and market data which altogether provide a unique view of the Chinese economy and at times, run against the consensus. The two then transition to a conversation on the Trump Administration, having a nuanced discussion on how tariffs and a reshaping of US trade policy affect both the domestic and global economy.

Economic Security and New Industrial Policy Asian Economic Policy Review

Abstract: The paper analyzes the emergence of Japan's economic security strategy to address the risks of weaponized interdependence in a context of heightened geopolitical tension. We detail the rapid institutionalization of economic security measures through the adoption of an Economic Security Promotion Act and ongoing reforms in areas such as foreign direct investment screening and export controls. We find, however, that Japan has made little headway in reducing its dependence on China for critical products, and export controls have had ambiguous trade effects. We discuss the role of the private sector in economic security and find significant divides by firm size on the uptake of new measures to address supply chain vulnerabilities and the protection of sensitive technologies. We examine the new industrial policy on semiconductors and point to the exigencies of success in fostering cutting-edge technologies. Our conclusion identifies policy challenges going forward and offers possible solutions.

Is inflation still slowing? Early 2025 data pivotal to outlook Federal Reserve Bank of Dallas

January inflation data were stronger in 2023 and 2024 than forecasters expected, even after more encouraging results had been reported for the ends of 2022 and 2023. Rather than reflecting seasonal adjustment difficulties, this pattern may be caused by a large share of firms changing prices at the start of a new year. If this is the case, first-quarter inflation data may exhibit greater persistence and sensitivity to swings in the business cycle. Whether early 2025 monthly inflation rates are similar to late 2024 or a repeat of the previous years’ surprises will be key to assessing the underlying momentum of inflation ahead

An Evaluation of World Economic Outlook Forecasts: Any Evidence of Asymmetry? International Monetary Fund

Using a large cross-country dataset covering over 150 countries and more than 10 macroeconomic variables, this study examines the consistency of IMF World Economic Outlook (WEO) forecasts with the full information rational expectations (FIRE) hypothesis. Similar to Consensus Economics forecasts, WEO forecasts exhibit an overreaction to news. Our analysis reveals that this overreaction is asymmetric, with more measured response to bad news, bringing forecasts closer to the FIRE benchmark. Moreover, forecasts align more closely with FIRE hypothesis during economic downturns or when a country is part of an IMF program. Overreaction becomes more pronounced for macroeconomic variables with low persistence and for forecasts over longer horizons, consistent with recent theoretical models. We also develop a model to explain how state-dependent nature of attentiveness may drive this asymmetric overreaction.

The Impact of Generative AI on Work Productivity Federal Reserve Bank of St. Louis Economy Blog

Generative artificial intelligence (AI) has rapidly emerged as a potentially important workplace technology. In an earlier blog post, we discussed results from the first nationally representative U.S. survey of generative AI adoption, conducted in August 2024. We showed that 28% of all workers used generative AI at work to some degree. We ran our survey again in November 2024 and found that usage rates were fairly stable between August and November. In this blog post, we leverage a novel question in the November survey to provide an estimate of potential aggregate productivity gains from generative AI.

Americas

How Does Latin America and the Caribbean View the Ukraine Conflict After Three Years of War? Ryan Berg/Center for Strategic and International Studies

Three years into the full-scale war between Russia and Ukraine, the conflict appears at an inflection point. The new U.S. administration of President Donald Trump has pledged to end the fighting and take the first steps toward negotiations with Russia. U.S. allies in Europe and beyond have, in turn, found themselves taken by surprise and decried what they see as a U.S. posture that is overly favorable to Moscow and potentially disastrous for Kyiv. For countries in Latin America and the Caribbean (LAC), a region which has, with few exceptions, sought to avoid taking strong positions on the conflict, the prospect of a ceasefire or peace agreement raises new questions, as well as opportunities for the region to assert itself on the global stage if it can take them.

With ELN Offensive, Colombia’s Security Crisis Has Come Roaring Back World Politics Review

Colombia now faces the worst security and humanitarian crisis it has seen in recent years, leading President Gustavo Petro to declare a state of emergency. Human rights organizations have raised concerns about the ELN’s conflation of civilians and EMB combatants. Indeed, it appears that the guerilla has especially targeted social activists and community leaders as well as those demobilized under the 2016 peace agreement.

IMF Loan to El Salvador Raises Transparency Concerns Center for Strategic & International Studies

In December 2024, El Salvador and the International Monetary Fund (IMF) reached a staff-level agreement for a $1.4 billion loan. The agreement, which outlines key policy commitments and structural reforms, remains subject to approval by the IMF Executive Board before the funds can be disbursed. However, concerns persist among civil society organizations and broader segments of the Salvadorean public that approval of an arrangement with the IMF could enable continued democratic backsliding and allow Nayib Bukele to further consolidate his authoritarian grip. The IMF Executive Board can help mitigate such concerns by enhancing transparency and accountability in the IMF-supported program. As a first step, including the following considerations into the IMF program would strengthen democratic norms and the rule of law in El Salvador, especially in the areas of governance and anti-corruption. Similarly, by improving consultation and encouraging communication with and the involvement of civil society actors, the IMF team, management, and the board would support broader public buy-in and strengthen program implementation.

Global Crime

Grand Theft Auto: Real Life Bloomberg/Business Week

When a car is stolen in the US, there’s a good chance that the thief is a teenager, and that the vehicle will end up in western Africa. Nowhere is international stolen-car traffic more robust than in the trade from the eastern US to ports in West Africa. With long-established routes hauling millions of shipping containers each month, car thieves have become bold in their efforts to slip stolen vehicles into this flow of legitimate commerce. Used-car brokers in West Africa know what models their customers will snap up, so they call US-based thieves to beef up inventory of highly desirable models – send orders for what they want to the US. All told, there were 1,020,729 car robberies in the US in 2023, the latest annual figure from the nonprofit National Insurance Crime Bureau.

Recommended Weekend Reads

The Power Requirements for AI Growth in the U.S., The Future of the USMCA, How Vietnam is Being Impacted By U.S. – China Trade Tensions, and How Russia Sees Trump’s Bid to Buy Greenland

February 7 - 9, 2025

Please find below our recommended reads from reports and articles we read in the last week. We hope you find these useful and that you have a relaxing weekend. And let us know if you or someone you know wants to be added to our distribution list.

Energy Requirements for Growing AI Capability

AI’s Power Requirements Under Exponential Growth Rand Corporation

Larger training runs and widespread deployment of future artificial intelligence (AI) systems may demand a rapid scale-up of computational resources (compute) that require unprecedented amounts of power. In this report, the authors extrapolate two exponential trends in AI compute to estimate AI data center power demand and assess its geopolitical consequences. They find that globally, AI data centers could need ten gigawatts (GW) of additional power capacity in 2025, which is more than the total power capacity of the state of Utah. If exponential growth in chip supply continues, AI data centers will need 68 GW in total by 2027 — almost a doubling of global data center power requirements from 2022 and close to California's 2022 total power capacity of 86 GW.

The Western Hemisphere

The Future of the USMCA Peterson Institute for International Economics

Since 2020, the last year of President Donald Trump’s first term in office, the often-quarrelsome trade relations among the three major countries of North America have been governed by the United States-Mexico-Canada trade agreement (USMCA). The pact must be renewed in 2026, but Trump has threatened withdrawing and imposing tariffs on Canada and Mexico, leaving the future of relations with two of the most important US trading partners uncertain. This guide explains why the agreement is under scrutiny, what’s at stake under different scenarios, and possible paths forward for negotiators if the current crisis is defused. This page will be updated as the trade deal is subjected to a new round of disputes and possible adjustments in President Trump’s second term.

Sheinbaum Isn’t Tempering Her Ambitions for Mexico’s Economy World Politics Review

Last month, President Claudia Sheinbaum unveiled “Plan Mexico,” an economic and development roadmap that aims to boost the Mexican economy through new public and private investments in a range of sectors, and new development-friendly policies. Among its principal aims are to create 1.5 million jobs in advanced manufacturing, increase investment as a proportion of GDP by 4 percent and grow Mexico’s economy from the 13th largest in the world currently to 10th by 2030. The plan is undoubtedly ambitious and comes at a time when the Mexican economy faces significant headwinds and uncertainty amid the threat of tariffs from the United States, as well as an overall deceleration of the economy, which grew at a modest pace of 1.8 percent in 2024, below the average of 2.4 percent for Latin America

Canadian Tariffs Will Undermine U.S. Mineral Security Center for Strategic and International Studies

As the United States races to reduce its reliance on China for minerals vital for national, economic, and energy security, tariffs with Canada may drastically undermine these efforts. Canada is the biggest source of the United States mineral imports, providing key sources of uranium, aluminum, nickel, steel copper, and niobium. To put it into perspective, in 2023, Canada accounted for $47 billion of United States mineral imports. China followed with $28.3 billion. The consequences of tariffs would be particularly profound for the defense industry, nuclear energy, and heavy manufacturing. A 25 percent tariff on Canadian mineral imports could cost U.S. off-takers an additional $11.75 billion—a figure that would increase as base metal and uranium prices recover. Canada would likely adopt retaliatory tariffs, as they did when Trump imposed Section 232 tariffs on steel and aluminum imports from Canada in 2018 and 2020 (backing down both times). In 2023, the United States sent $30.7 billion in minerals to Canada. The retaliatory tariffs could lead Canadian firms to pay an estimated additional $7.6 billion in tariffs, encouraging them to turn to other import sources for off-take, further undermining U.S. firms.

What Trump’s Trade War Would Mean, in Nine Charts Council on Foreign Relations

Although President Trump’s threated tariffs on Canada and Mexico have been delayed 30 days, what he has proposed could upend U.S. trade. These nine charts show what’s at stake, what comes next, and why it matters.

Trump’s Greenland Play: The View From Moscow The National Interest

The Russia-U.S. relationship (or lack thereof) has long dominated Arctic geopolitics. Geography makes the two neighbors and stakeholders sharing the challenges of a warming region. President Trump’s enduring interest in acquiring Greenland injects further potential geostrategic challenges in the region’s icy arena. When the idea was floated during his initial term in office, the immediate response from Russian leadership, state-operated media, and the public was a flood of memes. The second time around, however, Russia’s domestic discourse has a more strategic flavor. Discussions now appear to focus less on the “novelty” of such an acquisition and more on understanding the “objectives.” Three potential scenarios for U.S.-Greenland relations are being debated in Moscow in terms of the strategic implications for Russia.

Indo-Pacific

Factors Shaping the Future of China's Military Rand Corporation

China's population is declining, which will cause problems for China but not necessarily for the PLA. Fertility patterns in China are similar to those observed in other countries. This suggests that revoking the one-child policy will continue to have a smaller effect on population size than the Chinese government may have assumed, and that China's population will continue to shrink in the future. Despite this stark change, China's youth population will remain more than three times the size of the United States' youth population in the near term. China's current challenges include how to sustain economic growth as the economy matures and the population ages. Although demographic patterns in China are similar to those seen in other countries, comparisons should be made with caution; China's immense size means that small within-country changes could have large global impacts. The PLA's primary demographic challenge—which includes cultural, social, and political components—will be whether it can build and develop the type of military that Xi envisions.