Fulcrum Perspectives

An interactive blog sharing the Fulcrum team's policy updates and analysis.

Recommended Weekend Reads

Buying Greenland and Growing Arctic Security Risks, US Industrial Policy Toward Semiconductors Is Winning, and Demographic Decline in the US and Around the World

Please find below our recommended reads from reports and articles we read in the last week. We hope you find these useful and that you have a relaxing weekend. And let us know if you or someone you know wants to be added to our distribution list.

Buying Greenland & Increasing Arctic Security Risk

Everything you need to know about Trump’s Greenland gambit Atlantic Council

President-elect Trump is plotting an Arctic acquisition. As he prepares to take office on January 20, President-elect Donald Trump is already stirring up a transatlantic tempest with his overtures to acquire Greenland. Denmark has repeatedly said its strategically located island territory is not for sale, but Trump on Tuesday continued to push the issue—including threatening tariffs on Denmark. The icy dispute raises several burning questions. Atlantic Council experts have the answers.

Why Donald Trump wants Greenland: The Arctic Island has long been vital to US Security and its importance is only increasing Financial Times

When Trump first expressed interest in buying Greenland in 2019, he framed it as like “a large real estate deal” and emphasized the economic aspects of prising it away from Denmark. This time, his focus has changed. “We need Greenland for national security purposes,” he said on Tuesday, while mentioning the need to deter Russian and Chinese ships.

China-Russia Relations in the Arctic: What the Northern Limits of Their Partnership? Rand Corporation

To what extent might China and Russia form partnerships in the Arctic region, and what factors might limit the development of their relationship? Although the United States has had Russia as a maritime neighbor in the Arctic since 1867, the growing presence of China in the region as a Russian partner has led to a rare situation in which two competitive — and potentially hostile — states are in very close proximity to North America. In this paper, the authors evaluate Russia's and China's activities in the Arctic and these activities' implications for nations with Arctic interests. The authors consider China's decades-long interest in the Arctic, its growing and possible future economic activities, and the existing and proposed collaborations that Beijing has sought with Arctic countries to realize its goals.

Even in the face of widening Western sanctions, Russia managed to increase Arctic transit cargo by almost 50 percent over 2023. Its main Arctic shipping lane, the Northern Sea Route, recorded 97 transits carrying close to 3m tons of cargo; both figures surpassing previous highs. Total cargo volume along the route, including transits and traffic originating in Russia, stands at around 40m tons in 2024. Trade between Russia and China continues to dominate cargo flows, accounting for 2.9m tons or 95% of all transit traffic. Officials of the two countries met this week to discuss plans to further boost Arctic shipping.

‘Ice Sheet Conservation’ and International Discord: Governing (potential) Glacial Geoengineering in Antarctica International Affairs/Chatham House

There is a growing chance of collapse of the West Antarctic Ice Sheet, one of the planetary climate tipping points at greatest risk of being crossed. Such a collapse would subject the world to an increase of several meters in average global sea-level rise over just a few centuries. In this context, there is an academic debate about the potential of supporting glacial stability through artificial infrastructures such as an undersea ‘curtain’. However, this ‘ice sheet conservation’ would come with significant yet unforeseeable technical and environmental risks. Moreover, in this debate, governance risks have been either neglected or understated. We argue that the proposed infrastructures could negatively implicate the ‘peaceful purposes only’ obligation enshrined in the Antarctic Treaty. By affecting contentious areas of Antarctic geopolitics, such as authority, sovereignty and security, there is a significant risk that the project would make the Antarctic ‘the scene or object of international discord’.

Industrial Policy & the Race for Semiconductor Dominance

Industrial Policy through the CHIPS and Science Act: A Preliminary ReportPeterson Institute for International Economics

The 2022 CHIPS and Science Act appears likely to sharply boost the production of advanced semiconductors in the US, reducing the risk of future shortages but leaving America reliant on imported chips. The jobs created will come at notable costs. Some of the key takeaways of the report include: An estimated 93,000 temporary construction jobs and 43,000 permanent jobs will be created, at an average subsidy cost of $185,000 per job, per year—about twice the average annual salary of US semiconductor employees. Lawmakers deliberating the act did not publicly consider alternative ways of spending $200 billion to ensure adequate chip supplies. Additional subsidies will probably be needed to achieve the goal of producing 20 percent of global leading-edge logic chips in the US by 2030.

America’s bet on industrial policy starts to pay off for semiconductors The Economist (January 9, 2025)

In the final days of Joe Biden’s presidency, most parts of his administration are winding down. Not so the top brass in the Department of Commerce: on an almost daily basis, they are signing giant funding contracts with chipmakers, racing to dole out cash before Donald Trump enters the White House. When all is said and done, they will have awarded nearly $40bn to semiconductor makers in little more than a year—arguably the biggest single bet on industrial policy by the government in decades, and one that could end up as Mr. Biden’s most lasting economic legacy. The rush to disburse cash has invited questions about whether the funding commitments—the cornerstone of the chips and Science Act, passed in 2022—are at risk under Mr. Trump. On the campaign trail, he called chips a “bad” deal, saying the government could have just slapped tariffs on imported semiconductors. At the end of the day, Trump is unlikely to reverse the chip subsidies - but will he reinforce them?

Rationales for Industrial Policy in the Semiconductor IndustryIntereconomics

In recent years, private and public investments in the semiconductor industry have surged worldwide. In the European Union alone, a government subsidy package of €43 billion is under negotiation, while in the United States and East Asia, state support amounts to multiples of that figure. Economists view this subsidy race critically, as it could potentially lead to market distortions and inefficient allocations. In Germany, the substantial subsidies for new factories by Taiwan Semiconductor Manufacturing Company Limited (TSMC) and Intel are also the subjects of heated debate. Despite these concerns and the traditional reservations among economists against industrial policy in general, there are compelling reasons for pursuing such an industrial policy approach, particularly in the European semiconductor industry—provided the economic and political contexts are understood and the policy is well executed.

The Global Demographic Decline

The Demographic Outlook: 2025 to 2055 Congressional Budget Office

In CBO’s projections, the rate of population growth generally slows over the next 30 years, from an average of 0.4 percent a year between 2025 and 2035 to an average of 0.1 percent a year between 2036 and 2055. Net immigration becomes an increasingly important source of population growth. Without immigration, the population would shrink beginning in 2033, in part because fertility rates are projected to remain too low for a generation to replace itself.

Comparing Life Expectancies Across the Pacific Rim Visual Capitalist/Hindrich Foundation

Trade and economic growth have boosted life expectancy by improving access to healthcare and nutrition. Efficient resource allocation through trade improves living standards, and economic growth from trade raises income and tax revenues, enabling more government investment in public health and social programs. Based on the findings of the 2024 Hinrich-IMD Sustainable Trade Index, Visual Capitalist illustrates how major trading economies like Japan, Hong Kong, and Singapore enjoy higher living standards and longer lives.

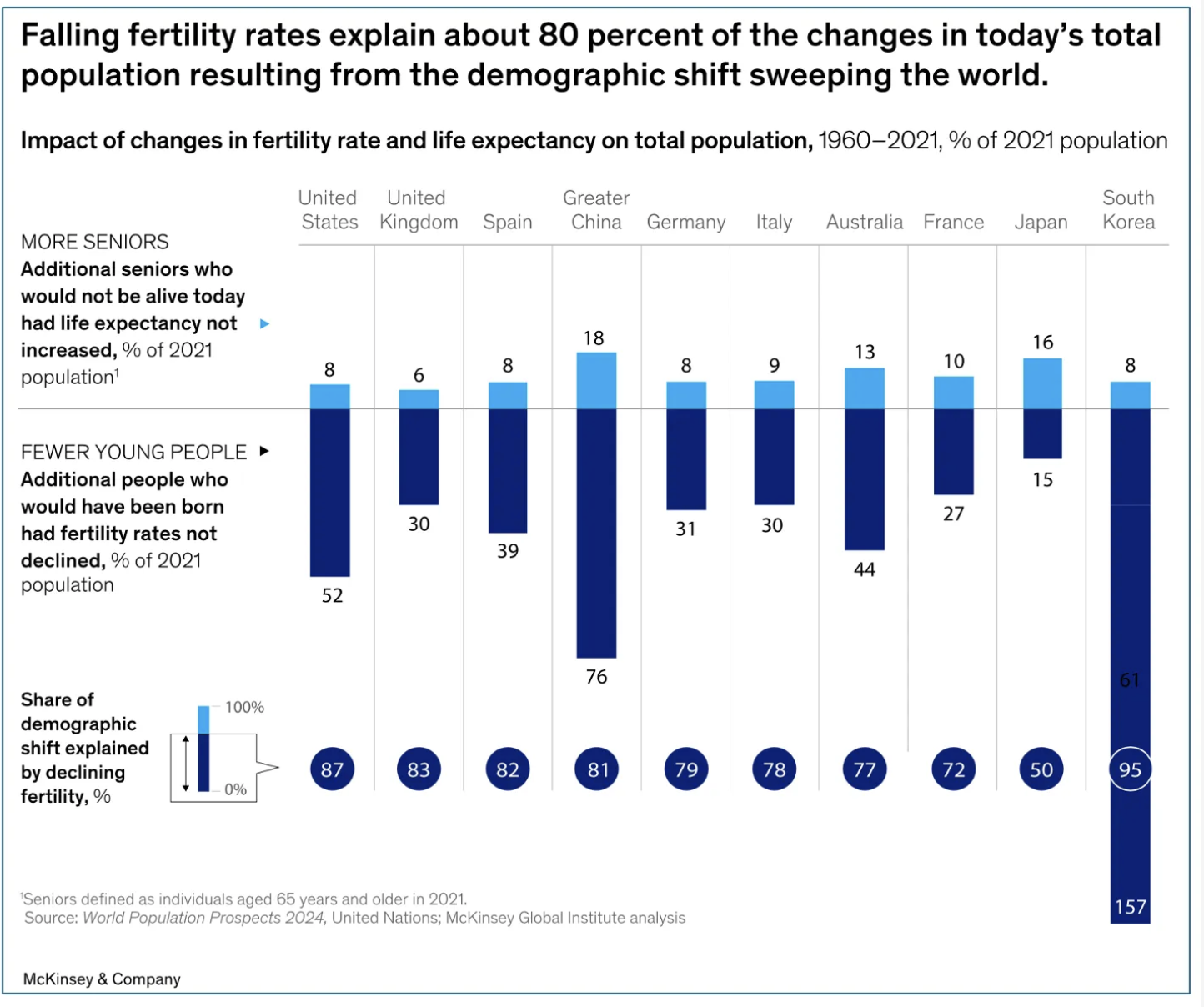

Dependency and depopulation? Confronting the consequences of a new demographic reality McKinsey Global Institute

Falling fertility rates are propelling major economies toward population collapse in this century. Two-thirds of humanity lives in countries with fertility below the replacement rate of 2.1 children per family. By 2100, populations in some major economies will fall by 20 to 50 percent, based on UN projections. Consumers and workers will be older and increasingly in the developing world. Seniors will account for one-quarter of global consumption by 2050, double their share in 1997. Developing countries will provide a growing share of global labor supply and of consumption, making their productivity and prosperity vital for global growth.The current calculus of economies cannot support existing income and retirement norms—something must give. In first wave countries across advanced economies and China, GDP per capita growth could slow by 0.4 percent annually on average from 2023 to 2050, and up to 0.8 percent in some countries, unless productivity growth increases by two to four times or people work one to five hours more per week. Retirement systems might need to channel as much as 50 percent of labor income to fund a 1.5-time increase in the gap between the aggregate consumption and income of seniors. Later wave countries, take note.

8 Billion of Us on Planet Earth…

According to the United Nations, the world’s population surpassed 8 billion this past Tuesday. While populations in sub-Saharan Africa are expected to continue growing substantially over the next 30 years, the annual global population growth rate is now at its slowest rate since 1950 – and moving into negative rates in many advanced economies.

One of the more interesting trends in global demographics is not getting much attention: India will become the most populous country in 2023, overtaking China. By 2050, it is estimated India's population will be 1.7 billion while China's population will shrink to 1.3 billion from its current 1.412 billion. In our view, the vaunted “China Century” is likely actually to be “the India Century.”

Subscribe to our newsletter.

Sign up with your email address to receive news and updates.